If a government bails out banks, it will most likely come in the form of preference shares which should rank equal to the existing ones that investors hold. However, the terms given to the government may be sweeter, along the likes of convertibility to shares at a premium to the current spot, callability at a premium to par, etc. similar to Buffett's terms with Bank of America.

So the chances of an outright default of any major European bank is unlikely. However, be prepared for some dividends to be missed and as a result, extreme price volatility. Expect drawdowns of around 40 - 50% in the worse affected banks. This is as bad a drawdown as with the ordinary shares. But for ordinary shareholders of affected banks, expect a total wipeout or the value to be decimated like ordinary shareholders of Bank of America, Citigroup back in 2009.

http://www.bloomberg.com/apps/news?pid=newsarchive&sid=aeIqWGr5Vnkw

Will Royal Bank of Scotland Continue to Pay Dividends on Its Preferreds?

Several readers asked me whether the newly nationalized Royal Bank of Scotland (RBS) will continue to pay dividends to owners of its non-cumulative preferred shares (and those of NatWest which it acquired).

My answer:

I do not know, but here is my best guess. the preferreds are a relatively minor part of the capital of the banks and are not currently being added to (like the common). So it is a free choice by the British PM Gordon Brown and and the Chancellor of the Exchequeur, Alisdair Darling, both of whom are Scots themselves, what they do about the biggest case, which is Royal Bank of Scotland. (Nat West is also RBS which acquired it before the mess hit.)

My guess is that they will not halt payment of interest on the preferred for a couple of reasons: 1) they were targetted at US retail investors, not speculative Britons like the recent buyers of RBS common; 2) the government wants eventually to sell the bank to the private sector again and does not want to hurt its standing too much; 3) this is a minor amount of money in fact; 4) it is linked to the dollar business RBS does, which is mostly wholesale, and cutting the payout would hurt the bank's global rep 5) the government's own shares are also preferreds which presumably means that preferred get preference which is what they normally get (I am not sure which preferreds are senior but in theory it is the ones we own) and 6) Britain would lose standing as an international bank centre if these payouts were halted.

They really don't want to wind up as Iceland on the Thames.

Another imponderable is news that the Dutch Parliament is looking into the acquisition by RBS of ABN-AmRo which triggered the meltdown at RBS and of course also hurt Dutch investors.

However, I have no deep insights into the souls of these Labourite Scots and I am just guessing. People can make stupid decisions based on a desire to control moral hazard, like the Paulson decision to let Lehman Brothers go bankrupt, which was a dreadful mistake.

That is why I say to buy the non-bailout bank preferred stocks too, which is Barclays (no UK govt. money taken or wanted, and a yield nearly as high).

There is a huge amount of speculative in- and out-flow into RBS and the other government assisted banks. There is risk with the preferreds but not in my view as much. I am buying these using limit orders, but am also keeping my fingers crossed. I will not comment on U.S. bank preferred stocks.

*Here is another view from an independent analyst at Datamonitor, Jonathan MacDonald, Lead Analyst writing on the British govt. bailout today: "damned if they do, damned if they don't". "It is not yet clear whether the move will prove successful as the current climate has no precedent' acknowledges MacDonald.

My answer:

I do not know, but here is my best guess. the preferreds are a relatively minor part of the capital of the banks and are not currently being added to (like the common). So it is a free choice by the British PM Gordon Brown and and the Chancellor of the Exchequeur, Alisdair Darling, both of whom are Scots themselves, what they do about the biggest case, which is Royal Bank of Scotland. (Nat West is also RBS which acquired it before the mess hit.)

My guess is that they will not halt payment of interest on the preferred for a couple of reasons: 1) they were targetted at US retail investors, not speculative Britons like the recent buyers of RBS common; 2) the government wants eventually to sell the bank to the private sector again and does not want to hurt its standing too much; 3) this is a minor amount of money in fact; 4) it is linked to the dollar business RBS does, which is mostly wholesale, and cutting the payout would hurt the bank's global rep 5) the government's own shares are also preferreds which presumably means that preferred get preference which is what they normally get (I am not sure which preferreds are senior but in theory it is the ones we own) and 6) Britain would lose standing as an international bank centre if these payouts were halted.

They really don't want to wind up as Iceland on the Thames.

Another imponderable is news that the Dutch Parliament is looking into the acquisition by RBS of ABN-AmRo which triggered the meltdown at RBS and of course also hurt Dutch investors.

However, I have no deep insights into the souls of these Labourite Scots and I am just guessing. People can make stupid decisions based on a desire to control moral hazard, like the Paulson decision to let Lehman Brothers go bankrupt, which was a dreadful mistake.

That is why I say to buy the non-bailout bank preferred stocks too, which is Barclays (no UK govt. money taken or wanted, and a yield nearly as high).

There is a huge amount of speculative in- and out-flow into RBS and the other government assisted banks. There is risk with the preferreds but not in my view as much. I am buying these using limit orders, but am also keeping my fingers crossed. I will not comment on U.S. bank preferred stocks.

*Here is another view from an independent analyst at Datamonitor, Jonathan MacDonald, Lead Analyst writing on the British govt. bailout today: "damned if they do, damned if they don't". "It is not yet clear whether the move will prove successful as the current climate has no precedent' acknowledges MacDonald.

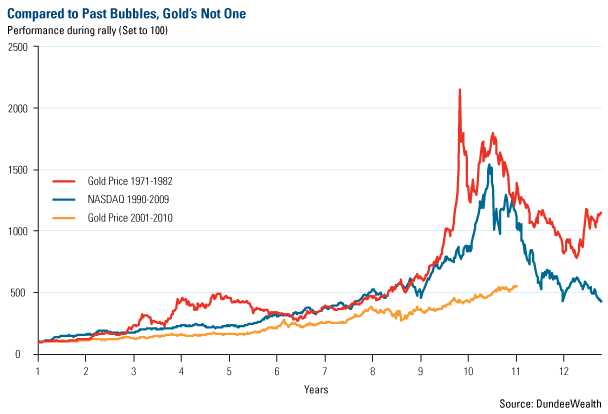

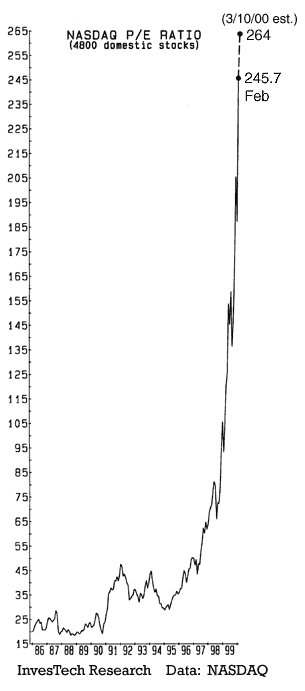

We do have a frame of reference for the internet bubble. You might remember that time as a period when everyone had a hot stock tip. Everyone was up hundreds of percent, or more, on companies like Cisco (

We do have a frame of reference for the internet bubble. You might remember that time as a period when everyone had a hot stock tip. Everyone was up hundreds of percent, or more, on companies like Cisco (