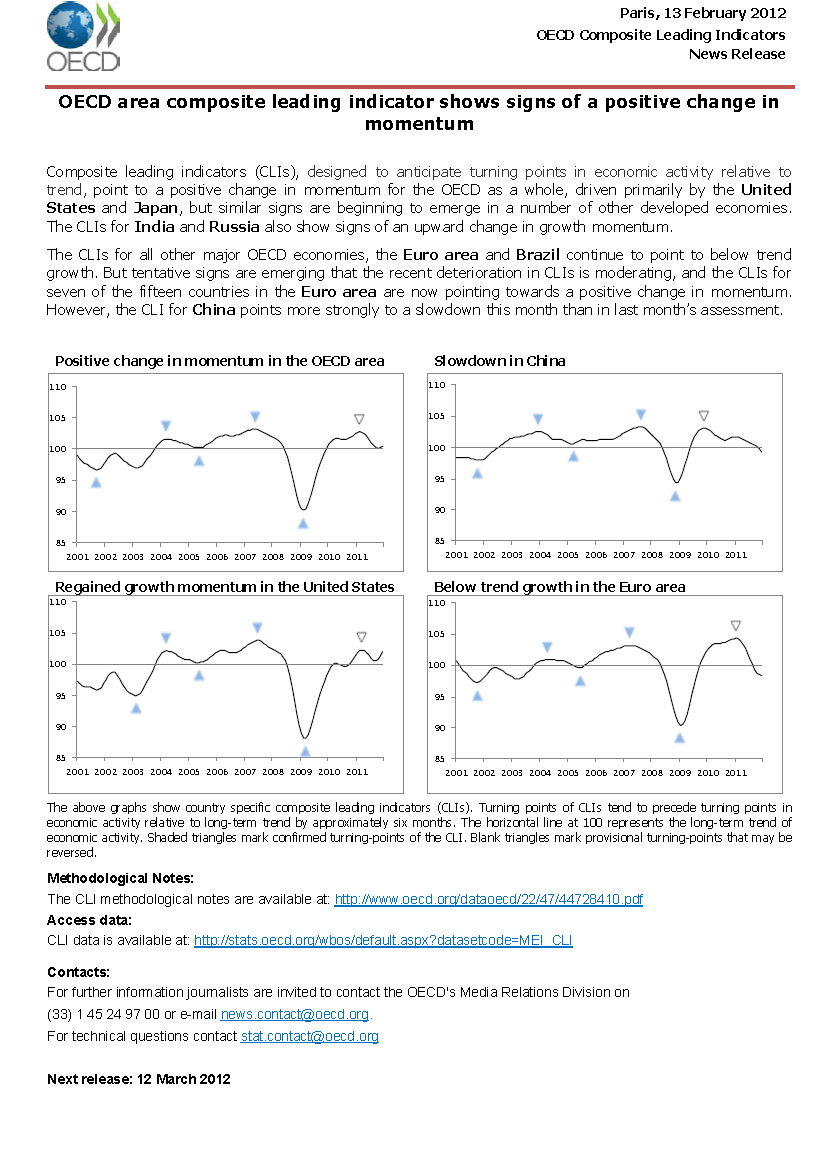

However, if the UK does enter into a recession, London properties are definitely more attractive than Singapore's, from a lifestyle perspective, because you get to live in one of the most sought after cities in the world, where you are just minutes away from West End Theatres, famous Michelin restaurants, the majestic historical buildings, and the lovely River Thames. What's more, London's retail prices, restaurant prices are now equal if not cheaper than Singapore's. The power of the SGD has made us more internationally mobile now.

The most attractive properties right now is in the US. It is still falling and is near the bottom of the cycle, unlike in Singapore and UK. The fall in prices vary widely, from New York and the north eastern states which fell less than 35% from the peak in 2006/07, to more than 70% in Las Vegas and Florida. Marc Faber, Donald Trump and Warren Buffett have said recently that US properties is worth buying now, so I will be looking at them soon. The tax laws are complex. There are capital gains taxes and property taxes, unlike in Singapore.

Published February 23, 2012

| |||

Sparkle in prime London homes

Top notch residential property defies recession and rises in 2011, reports NEIL BEHRMANN

(LONDON) Prime residential property in London defied the gloomy British economy and achieved sharp gains in 2011.

The eurozone crisis and Middle Eastern revolutions turned out to be bullish for prime properties priced anywhere between £pounds;500,000 (S$1 million) and £pounds;20 million (S$40 million) or more. Money flowed from Italy, Greece and Egypt, according to agents, while Russian and other billionaires and multi-millionaires continued to favour the city. Such money tended to head for Knightsbridge, Kensington, Mayfair, Chelsea, Regents Park, St John's Wood, Hampstead and other prime London boroughs. Price changes of other London boroughs, on the other hand, were mainly mixed with small increases and declines. The index is below the August 2011 peak, which was a new record, but it fell back and in December was 4.6 per cent below the 2008 pre-recession peak. The performance of large prime area flats over 1,500 sq ft has been staggering. In 2011, the apartment price index jumped by 24.9 per cent and was up by 64.5 per cent from the 2009 nadir. Indeed, the appreciation matched the revival of the FTSE 100 from its 2009 depths. The difference, however, was that the real estate rise took place on very low volumes. Following such a run, gross yields on rentals have tumbled to around 3.3 per cent on apartments and 2.9 per cent for houses. James Wyatt, head of valuation at John D Wood, estimates that after deducting agent and management fees, maintenance, other charges and tenant voids, net rental yields can be estimated at only 2.3 per cent for flats and 2 per cent for houses. The low returns indicate that the prime market has become over-blown for investors, although foreign super-rich buyers and others sought London homes for a variety of other reasons. Some of the money reportedly entered the market to evade taxation, though this could not be confirmed. Regardless of the reasons for purchase, London prime real estate has become far more pricey than depressed US city properties. 'The cardinal rule is to be highly selective,' says Michael Ross, head of Stockton Estates, a London-based commercial and residential property company. He is wary of ultra low rental yields, but notes that since property is a non-homogeneous market, careful buyers can find opportunities to refurbish units and boost valuations. The UK Land Registry's sales data to end November 2011 shows the wide price differential between London areas. Average prices in Kensington and Chelsea of around £pounds;950,000 compare with outer areas, such as Sutton and Croydon of around £pounds;240,000. Gross yields on properties of lower priced London boroughs range between 4 per cent and 6 per cent, but high maintenance and wide tenant voids can slash the net yield below 3 per cent, caution agents. The London property market faces a year of considerable uncertainty in a nation which is experiencing recession and high unemployment. Despite a stock market rally late December, January and February, trading, initial public offering and merger and acquisition volumes have shrunk. Widespread layoffs are occurring in the City of London and bonus payments have fallen. 'The raft of City job losses announced in recent weeks is a reminder that London will not escape the recession unscathed,' says Ed Stansfield, head of property research at Capital Economics. On the face of it both prices and rentals could slip although demand from overseas buyers could support prices in the short run. London, however, is likely to underperform on a medium-term view because valuations are stretched, he maintains. Drivers Jonas Deloitte's latest London Residential Crane Survey found, however, that large numbers of developments will be completed this year. The more buoyant market raised construction levels to 39,300 units within 247 development schemes. Drivers Jonas Deloitte's unconventional research, which counts the number of cranes on residential schemes with 50 units or more, concludes that new build real estate in the pipeline is heavily dominated by flats, which account for 95 per cent of all units. Liam Bailey, head of residential research at Knight Frank, forecasts that London prices will fall by 3.7 per cent in 2012, but that prime area prices will still manage to increase by 5 per cent. The firm believes there is a 75 per cent chance that conditions in the UK mainstream market over the next few years 'will resemble a slow correction under which the market will experience an extended period of low transaction numbers and price falls in real terms'. It contends that there is a 20 per cent chance of a sharp fall, similar to the 2008/2009 property bear market, if there is a severe sovereign debt crisis, a collapse of the euro or an unexpected rise in interest rates. | |||