http://www.propertybuyer.com.sg/articles/singapore-property-investor-buyer/singapore-property-buyer-august-2010-outlook/

Singapore Property Buyer August 2010 outlook

The market has risen from dramatically from June 2009. Within 3 months from June 2009 to Sep 2009, the market went crazy. Between Sep 2009 to July 2010, Singapore property prices continued to move up.

By the 1Q, 2010, landed property in Singapore has reached 175.0, Non landed property has reached 174.5. (URA price index 1st Quarter 2010)

Rising by 8.3% for landed property between 4Q, 2009 and 1Q, 2010, condominiums rose another 5.7% between 4Q, 2009 and 1Q, 2010.

Source: URA

As we write, prices of properties such as Aspen heights have hit $1600 psf, Leonie Studios hit $1600 to 1700 psf, 76 Shenton reached $2100 psf, Waterfall Garden $1730 psf, Cyan at $2400 psf, Ardmore Park and Ardmore II have reached $2500 to $3000 psf.

Even mass market condominiums are approaching or have breached $1000 psf. Many mass market developments such as The Waterina are going for $900 to $1000 psf. Even the Atrium Residences within Geylang is going for $700 to $800 psf.

Effects of Share market on sentiments

The share market has also recovered to about 3000 points on the Straits times index.

The share market has also stagnated since late last year. The share market usually leads the property market by 3 to 6 months. However it would be quite hard to predict property prices based on the share market as this time round, this time round, the covariance may be less (but to be verified). The property market's rise is due rather to the under-supply of HDB flats which supports price rise.

Throughout this recession in 2008 and 2009, Singapore expatriates are the least affected in terms of job losses compared to locals (Ministry of manpower). And there has been a quick return of expatriates through job recovery in Singapore. This supports rental as well as mid to high end property market.

Many studies have found a positive correlation between the share market prices and property prices. As this share market wealth cannot fully account for raising funds for down-payment of properties or raise long term affordability in terms of earning capacity, therefore we conclude that it is sentiment driven as many analyst have concurred before us.

CREDIT, LIQUIDITY, MONETARY AUTHORITY AND SINGAPORE BANK’S INTEREST RATES

Singapore's market has no lack of credit given the low bank interest rate environment, so what supports the prices and transaction volumes are in many cases consumer confidence.

Therefore when there are positive press spins, news reviews and or awareness of certain property launches or economic projections which accentuates the possibilities (regardless of whether it is well grounded in facts or not), the property awareness and demand appears.

Recently, the deputy Managing Director of Monetary Authority of Singapore Mr. Ong Chong Tee has come out and clarified that the Sibor’s dropped in interest rates is no cause of alarm as this is due to a change in MAS’ Singapore currency stance going from Neutral to Appreciation against our major trading partners. As a result of this change in stance, smart money flowed into Singapore in anticipation of currency appreciation of the Singapore dollar.

The previous time in 2008 when interest rates suddenly fell, it was due to a looming recession. We at Property Buyer Singapore Mortgage Consultants are satisfied with the explanation and are happy that there was an explanation from Mr. Ong of MAS.

However we are still unclear why Monetary Authority of Singapore wants to change Singapore’s currency stance to “Appreciation”. Does MAS foresee food and commodities inflation?

Does MAS foresee turbulence in the surrounding countries and are instead using monetary policy as a means to maintain liquidity in the Singapore banking system?

Risks for Singapore Property buyers and investors

The risk to Singapore property buyer is becoming elevated. Based on URA's price index, the prices now are even higher than the previous peak in 1996. This means that, there is no more guidance going forward as we moved into uncharted territory. Where the market will go is fairly uncertain. The market will not only behave in accordance with supply and demand, but will also take it's cue from the local domestic economy as well as what is happening in the world, such as the from the USA, China and Europe.

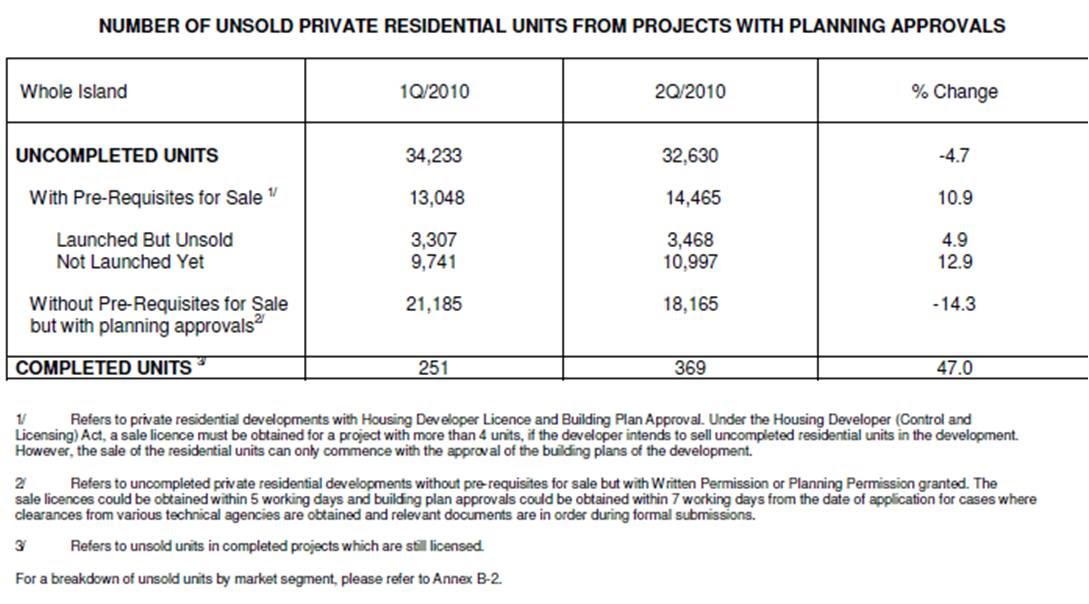

Mass Market Condominium Prices and outlook

The mass property condominium market will be guided by supply and demand of HDB housing. This is expected to continue it's ascent, although at a slower pace. Huge supply shortage by HDB coupled by a massive immigration policy has created a huge problem of rising property prices right from the base level of HDB. However, do note that there are still some 61,000 units of private residential supply in the pipeline up till 2015 and more than 30,000 of unsold units out of that 61,000 units.

High End Luxury Market Property outlook

The high end Luxury Market, it is more often guided by prices of the best properties in each of the advanced economies.

This market is often defined by superlatives such as, the best, the tallest, the best view, the nearest, the most exclusive and etc.

As the Singapore property market has reached a peak that is never before reached since 1996, the high end luxury market can be a bit lost for direction. This can cause nervousness when the market is not exuberant.

We feel that the government fears that the super high end luxury market will soften. The government (through the state media) has always taken pains to point out that despite the super high Per square feet prices (psf) reaching ever new heights, it is still cheap compared to Hong Kong, Tokyo, London, New York and Paris, other global cities.

And high end luxury properties in Singapore has seen keen interests from Singapore expatriates as well as super high net worth foreigners parking their money here or buying another home in this part of the world as part of their travel itinerary.

The areas categorized by high end luxury properties are: -

Ardmore park, Grange road, Leonie Hill, Oxley Road, Patterson road, Botanical garden area, st. Martin, Balmoral road, Marina Bay, Sentosa Cove and etc.

Of these, Marina Bay and Sentosa cove are new entrants to the luxury market, the rest are the traditional District 9, 10 and 11 areas. There are more high end luxury properties that may be launched in the coastal areas such as Keppel road, Shenton Way. All are masquerading as a potential high end luxury property candidate, but not all will have the attributes befitting that of High end luxury properties. Therefore buyers need to be careful to identify the genuine High End luxury properties.

Super high end Luxury properties have been characterized by high price volatility

The difference could be between paying $4000 psf versus $2500 psf. For those people who are adequately rich with $5 to $10 million in net assets, this could be the investment that hurt their net worth if they buy at the wrong time. For those with $20 to $100million, there is substantial holding power, therefore whether they take it as an investment or consumption, it doesn't really matter.

This segment of rich high net worth individuals come and go in droves depending on policies of their home countries such as tax treatment as well as economic cycles. The price premium given for frills and property features may be severely compressed during bad economic cycles.

Super High End Luxury Property rise create head-room for the Mid end luxury market

Mid end luxury markets are defined as those in outer central region. Typically those in the fringe of District 9, 10 or 11. These properties are currently in the price range of $1100 to $1500 psf. With the price ceiling of properties such as Leonie Studio at $1700 to $1800, 76 Shenton at $1800 to $2000 psf range, it will be hard for the mid end properties to rise above $1600 psf. Therefore, the top of their pricing range would likely be, $1600 psf while the median and mean prices are likely to gather closer together at $1300 to $1400 psf as the mass market condominiums are already closing in at $1000 to $1100 psf for 99 years properties in traditionally non prime areas.

Singapore Property Owner and Buyer's Holding Power

Employment figures are firm and is unlikely to throw a spanner in the works as there is only 2.2% headline unemployment as at Mar 2010 (source: Ministry of manpower). There is still a shortage in HDB supply. While land is being released for sale by the government, the physical property shortage is not immediately eased.

Therefore as long as property buyers are going in with reasonable prices and not over-bid, then the likelihood of being caught off guard in a sudden downward spiral of prices is limited. This would mean that property buyers would be better off to bid within the median of valuations.

The prices for properties in Singapore (in general) should still hold firm. However this may not hold true for certain high price volatility developments or projects where large swings are possible.

HIGH END PROPERTY MARKET Versus Mass Market

The high end market should still hold firm, perhaps with potential to appreciate. Those properties very near to the high end market should trend upwards if such high end market firms up.

Properties with attributes that matches the best of it’s kind worldwide will have a price benchmark comparable to the best properties in internationally well known locations. Such amenities may include very exclusive attributes such as Yatch berthing, Helipad, panic room, sea view, special butler service, near to resorts, town and financial centres, centres of activities and entertainment, port access, private lift lobbies, super high ceilings, golf, infinity pools, security service, near to expat schools, and special immigration and residential rights in some countries or superlatives such as highest, tallest, most luxurious, or certain design attributes that puts them amongst the very best worldwide.

When high end market moves upwards, this creates increased head-room for the properties one grade below the high end market to move upwards.

The rises may then ripple out throughout the country. If the rises at the high end market are highly selective, such positive price rises led by high end market may not fully ripple throughout the country. This will widen the price gap between the mass market and the high end luxury market.

Mass market and High end markets are properties belonging to different worlds. The mass market is characterized more by affordability while the high end market can defy gravity to some extent. Therefore we can say mass market properties are sensitive to affordability and general income conditions.

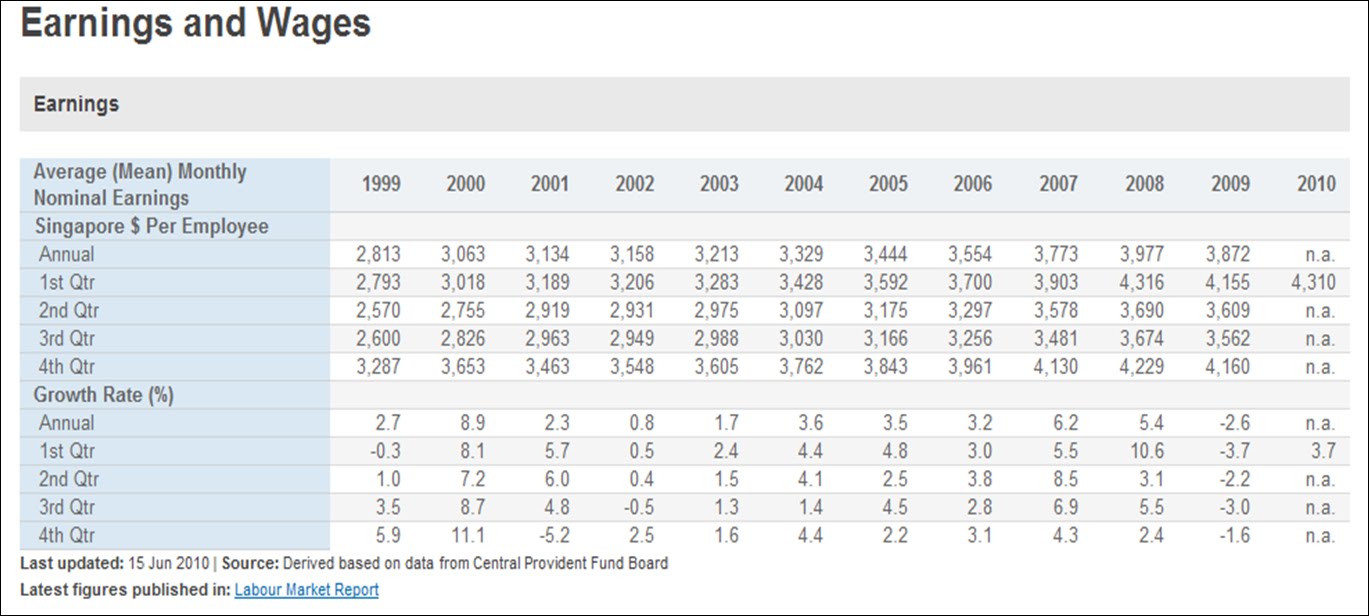

Source: Singapore Ministry of Manpower, aggregated from Central Provident Fund board

The average (mean) monthly nominal earnings are around $4000 in 2010 (our estimate) per person $3,977 in 2008 and $3,872 in 2009 (Ministry of manpower). So an average house hold will have $8000 household income assuming a 2 person household.

So an average couple with $8000 income (with no current liabilities)

30 years housing loan tenor

50% debt servicing ratio

2% interest rates

The maximum affordability works out to be roughly $1.082m.

This means that the average Singapore household can afford a property of $1.35m. (If they can find the money for the downpayment) – A typical aggressive Singapore bank.

For a more conservative bank in Singapore, it may set the interest rate threshold at 3.75%, thereby reducing the loan size to $863,000 of loans.

This means that the average Singapore household can afford a property of $1.08m.

Since ministers and rich businessmen heavily skew the average salaries upwards, so the median salaries should be much lower. According to the Singstat, the median house hold income was $4,850 in 2009 (Singstat, http://www.singstat.gov.sg/news/news/op19022010.pdf ) and when median income was sorted by property type, house hold income of “$12,500 for private flats, condominiums and private houses in 2009” (Singstat, http://www.singstat.gov.sg/news/news/op19022010.pdf)

Singapore's Average household pay = $8000 (15 june 2010) – based on 2 x $4000 per person (2 to a household)

Singapore's Median Household pay = $4850 (based on 2009 figures)

So there is considerable income disparity in Singapore.

Since current private condominium owners have a household income of $12,500, so if we lower the entry barrier for private condominium purchase to $8,000, what will happen?

Assuming that the average household income at $8,000 who are not eligible for HDB “subsidized” property prices would like to upgrade to a condominium, these group of people if they have already an HDB would have a Cash-over-valuation amount which helps them to pay the downpayment. If these people are buying for the first time, they would be able to afford properties of between $1.08m to $1.35m at the maximum.

Based on an average small family nucleus of 2 person, such a family would stay in condominiums of around 800 to 1100 square feet. At $1m to $1.1m (using more conservative figures), this would represent an affordability level at $909 psf to $1,375 psf depending on the size of the unit purchased.

The likely property price effect is: -

HDB supply crunch leads to price increase in HDB.

HDB price increase leads (to some extent) to upgrading to mass market condominium (funded by HDB sales profits)

Direct purchase of condominiums skipping HDB altogether with an income level of $8,000 (per household), the affordability level can support property prices at $909 psf to $1,375 psf range (say 800 sq feet to 1100 sq feet).

Unfortunately, due to the fact that you can afford it, it will also be good reason for the Singapore government to raise prices of land and pass on the cost to the property developers who will then pass it on to you. Mass market singapore private properties may even possibly reach $1200 psf range, simply because you can afford it. (if employment holds stable and GDP is growing)

“ Among employed households, median household income from work was $1,090 for those in HDB 1- & 2-room flats, $3,190 for HDB 3-room flats, $5,560 for HDB 4-room or larger flats, and $12,500 for private flats, condominiums and private houses in 2009, lower when comparing with 2008.” (Singapore Department of Statistics Press Release, 19 Feb 2010)

In our previous research (Search for “Why HDB prices go Crazy” http://www.propertybuyer.com.sg/articles/singapore-property-investor-buyer/why-singapore-property-prices-go-crazy/) That craziness is due largely to lumpy supply and less than perfect timing by the Singapore government. This under-supply of properties lead to massive prices increase when sentiment is positive and affordability is achieved. This augurs well for the government coffers for land sales which help the government raise money so as to be able to run a budget surplus during this current 5 year term of PAP rule and hence able to give our election goodie bags.

However the Singapore government releases of more private land for building of condominiums creates more potential over-supply in the private residential market which needs to be absorbed by genuine property buyers.

Overall the risks for high end properties and mid to high end properties lies in it’s price volatility during market swings.

The risk in mass market condominiums lies in affordability and that of losing employment. At current elevated prices, if employment figures holds up, a new price benchmark is formed. Such new prices will likely hold firm. The mass market condominium is supported by HDB which is still currently in short supply. HDB forms the price basement for all mass market condominiums.

Note: Limitations in this assumption lies in it's looking only at loan serviceability and ignores cash downpayment portion. Using national savings as a guide would be misleading as the savings and cash holdings are not homogeneous across the country and not across all income groups. So for simplicity, we ignored the cash downpayment funding portion. However we do acknowledge that HDB profits can come up to $100,000 to $300,000 in some cases which can easily fund private properties 20% downpayment.

Some valuation and current prices (condos) in Shenton Way (ref: URA caveat): -

76 Shenton – between $1,900 - $2,400 psf.

The Sail @ Marina Bay - between $2,000 - $3,300 psf

International Plaza $1,100 range

Icon $1,600 - $1,700 psf

Some parts of China town, Tiong bahru, etc….

Leonie Hill, Leonie Studio $1,500 to $1,900

Grange residences $2,500 to $2,800 psf

Ardmore park $3,000 - $3,600 psf

Balmoral $1,500 - $1, 800 psf

Cyan Bukit timah (New development) $1,800 - $2,400 psf

Aspen heights $1,400 - $1,600 psf

Rivergate $1,600 to $1,900 psf

5th Avenue Condominium $1,200 to $1,400 psf

Singapore BANKS CREDIT stance

Banks have generally been more forth coming in their loans and loosened credit. Banks such as Citi banks which were burnt badly in the sub-prime crisis and was largely dormant has come to life with the introduction of an aggressive package SIBOR + 0.5% ascending to 0.9% in June 2010.

HSBC has also woke up from their slumber from around Feb 2010. And Bank of East Asia is starting to jump into the fray of residential housing loans.

Banks are starting to lend more freely.

Since banks are willing to lend more freely, we suggest you take more caution instead of letting your guard down. As property market comes in phases, do your own home work.

Effect of Global Market on Singapore property prices.

(Source: wikipedia, 2009, http://en.wikipedia.org/wiki/File:Nominal_GDP_IMF_2008_millions_of_USD.jpg )

Europe

A collective austerity measure by Europe may spell disaster for the world economy as it is the biggest economic bloc in the world. Although Europe can no longer spend more than they earn, but tightening at such a stage in the name of balancing the budget while noble is probably not the way to go about it. But neither is spending it’s way out of recession.

Spending cuts should be cut at segments that adds little job creation value. If UK and Germany cut public spending where private sector depended upon, this may further hurt private enterprise and shed more jobs. Europe may further look inwards and reduce trade with the rest of the world given this self imposed austerity drive.

Hopefully there are pockets of liquidity amongst the wealthy which certain policies can help bring such wealth into the path of consumption and thence job creation.

USA

After about 1 Trillion US dollar of stimulus, the economy seems to have stabled. And with that, it sends a stabilising signal to the rest of the world. However we are now reaching the tail end of the stimulus package which was first launched on Dec 2008 by President Obama. Economic recovery has been tentative at best. New fiscal stimulus may not be forthcoming given the massive budget deficit.

Many states are unable to balance their budget and depended to issuing municipal bonds to fund their deficits.

Source: http://www.tradingeconomics.com/Economics/Interest-Rate.aspx?Symbol=USD

The US has kept their Federal Reserve overnight interest rates at 0.25% for more than 1 year now. It is fairly certain to say that part of this cheap borrowing has benefited home owners and businesses, but part of it will certainly have flowed overseas as a “Carry Trade” activity where borrowers borrow at cheap rates and convert it to a higher yielding investment in another country. It is difficult to track how much of these funds are operating overseas.

It is also similarly difficult to estimate how much funds banks and other financial institutions have in order to lend out to help set the overnight benchmark interest rates as the federal reserve gradually winds down setting such a low interest rate as it's funds are gradually depleted. Without the Federal reserve's involvement, the benchmark interest rates will almost certainly rise.

CHINA

China is a growth engine and an export engine. And this economy is showing signs of increase in consumption. China has a massive surplus and foreign currency reserves estimated to be worth more than US$2 trillion dollars. The biggest in the world!

China funds the consumption by the united states as well as Europe. As long as China continue to fund the US and Europe, these governments can for the time being issue more bonds and hope that China and various cash rich sovereign funds buy their bonds so that they can continue to finance the deficit. Issuing bonds while at the same time creating extra money supply is not the best way, but it is still better than issuing more money supply without a corresponding debt or higher tangible asset value of the currency.

China's hot property market has become highly speculative. The rental yield of china's properties are very low, there is practically no rental value for many of these properties with sky high prices. Many are vacant. These is surely a bubble or what they would call, a musical chair, where one hopes to pass it on to the next person for a profit.

Assets that do not generate a yield are not assets, they are liabilities. We don't know when this situation will burst, but if and when it does, it could have ramifications across Asia. Chinese high net worth people who are burnt may start to unwind their investment holdings in the rest of Asia. This could be a potential and damaging negative economic headwind for Asia.

Singapore's Macro Economy

We are skeptical of the real strength of the Singapore economy. Despite the GDP's high growth, it is coming from a low base due to the prior recession and it is not entirely an efficiency led growth, but rather an immigration and investment led growth.

A demand led growth is more sustainable in our opinion. But that is not entirely within Singapore's government control.

Singapore per capital GDP would be pretty much the same, but as a result of massive immigration, the overall nominal GDP values will grow as expatriates and immigrants need housing, schools, food, services, etc.

Hence we expect that property prices will continue to ascent at a slow rate all the way towards end of 2010. And risks for property buyers will increase. However it is too early to guess when this property rally will end. If a property buyer is genuinely looking for somewhere to stay, they would still have to do so sensibly and quickly.

If a property investor is looking for investments, they may have missed the best part of the recovery story. If their time horizon is long, it would be prudent to wait a few years to time the market when the market is flooded with properties developed from Singapore's government massive land sales program now. But there is no guarantee that there will be a crash in the market as the Singapore government could always resort to bringing in even more foreigners to find demand for housing and therefore support high land prices.

SUMMARY (Assuming no massive fall-out from the global economy)

HDB – Prices to rise

Mass market – Prices to rise

Mid Tier – May rise

High End Luxury Market – Uncertain