I've written stuff that I feel may hurt some people's feelings. Even if the comments I've made were true, it's no point talking about the past but to look forward. I'll forgive and forget. If I've offended anyone, I hope I'll be granted the same mercy too. I'm amending this post to prevent any hurt that I may create from my comments.

I realise that I need both engines (EQ and IQ) to fire. An ex-boss once told me, "why bother to do CFA, you're now so old". He could not even clear level 1. This is the kind of people that harms others. Some bosses use their charm and nothing else... It's a shallow world and the likeable people get the rewards.

Where's the justice?

Sometimes I wished that I'm a charmer as well. But I am different. I am capable of driving the business side of things. I am capable of handling people. I am capable of looking at the markets and making a call.

I wish to have a heart as well. I want to have patience, to listen more, to analyse more before judging. to have compassion, to empathise. I need sharpness to hit the problem at the nail and at the same time leave room for doubt. I have to change my approach to talking to people... to know what's on their minds, their worries, their agenda, so that I can forge a win-win solution.

Indeed, I will love all, serve all.

Saturday, 30 April 2011

Gold-Buying Central Bankers May Extend Record Rally

My opinion is: gold is likely to shoot up at least another 10 - 20%, reaching USD1600 - 1700/oz before pausing in 3rd or 4th quarter 2011 when the Fed starts to hike rates. It may correct to USD1500 for half a year before resuming its rise in first half of 2012 when inflation spirals out of control worldwide. It could hit USD1800 - 1900/oz, suggesting a 25% upside before the world's stock markets start to fall in 2nd half 2012. Gold will probably correct 35% to around USD1400 oz in 2013.

Gold-Buying Central Bankers May Extend Record Rally

By Pham-Duy Nguyen - Apr 29, 2011 12:00 PM GMT+0800

Gold prices reached a record 14 times this month on demand from investors seeking an alternative to the dollar after the currency slumped to the lowest since 2009, U.S. debt widened, and the Federal Reserve signaled April 27 that borrowing costs will remain near zero percent for an extended period.

Central banks that were net sellers of gold a decade ago are buying the precious metal to reduce their reliance on the dollar as a reserve currency, signaling demand that may extend a record rally in prices.

As developing countries accelerate purchases, gold may reach $2,000 an ounce this year, compared with a record of $1,538.80 yesterday in New York, said Robert McEwen, the chief executive officer of producer U.S. Gold Corp. Euro Pacific Capital’s Michael Pento, who correctly predicted gold’s highs for the past two years, forecast a 2011 high of $1,600.

Prices reached a record 14 times this month on demand from investors seeking an alternative to the dollar after the currency slumped to the lowest since 2009, U.S. debt widened, and the Federal Reserve signaled April 27 that borrowing costs will remain near zero percent for an extended period. The economy in China, the biggest foreign holder of U.S. Treasuries, grew 9.7 percent in the first quarter.

“China is out to have more gold than America, and Russia is aspiring to the same,” McEwen said yesterday in an interview in New York. “When you have debt, you don’t have a lot of flexibility. China wants to show its currency has more backing than the U.S.”

In 2010, central banks became net buyers for the first time in two decades, adding 87 metric tons in official-sector purchases by countries including Bolivia, Sri Lanka and Mauritius, according to World Gold Council data. China, with more than $3 trillion in foreign-currency reserves, plans to set up new funds to invest in precious metals, Century Weekly reported this week. Russia purchased 8 tons of gold in the first quarter.

China’s Gold Reserves

China, which has just 1.6 percent of its reserves in gold, may invest more than $1 trillion in bullion, Pento said. “China wants to be an international player, and they need to own more gold than they currently have.”

The U.S. Treasury Department projects the government could reach its debt ceiling of $14.3 trillion as soon as mid-May and run out of options for avoiding default by early July. The Fed has kept its benchmark rate between zero percent and 0.25 percent since December 2008 to help stimulate the economy, driving the dollar down 11 percent against a basket of six major currencies during the past year.

“Until monetary policy changes, you’re going to continue to see gold go up,” said Michael Cuggino, who helps manage $12 billion at Permanent Portfolio Funds in San Francisco.

“Ultimately the best thing we can do to create strong fundamentals for the dollar in the medium term is first, keep inflation low, which maintains the buying power of the dollar, and second, create a stronger economy,” Fed Chairman Ben S. Bernanke said on April 27.

U.S. Reserves

As of April, China was the sixth-largest official holder of gold, with 1,054.1 tons, according to World Gold Council estimates. The U.S. has the most, with 8,133.5 tons, or 74.8 percent of the nation’s currency reserves, council data show.

Central-bank buying may have the same impact on gold as the introduction of exchange-traded funds, Cuggino said. Prices have more than tripled since the SPDR Gold Trust, the biggest ETF backed by bullion, was introduced in November 2004.

Central banks in emerging markets may aim to hold 2 percent to 8 percent of their foreign-currency reserves in gold, Francisco Blanch, the head of commodities research at Bank of America Merrill Lynch in New York, said in an interview.

Gold is “close to” its cyclical high, said Blanch, who expects the metal to average $1,500 this year.

Gold’s Enemies

“The enemies of gold are rising interest rates and a balanced budget,” said Pento of Euro Pacific Capital in New York. “I look for a summer swoon once Bernanke exits the bond market. You’re going to have a temporary rise in real interest rates.”

The Fed said it would buy $600 billion in U.S. Treasuries through June.

The Federal Funds rate would have to rise to “Volcker” levels before gold enters a bear market, said Gold Corp.’s McEwen, who expects the metal to rise to $5,000 over three to four years.

Prices have advanced 7.7 percent this year, extending a decade of gains in which gold jumped sixfold from a low in 1999. The all-time inflation adjusted record is $2,338.92, based on the value on Jan. 21, 1980, according to a calculator on the Web site of the Federal Reserve Bank of Minneapolis.

Former Fed Chairman Paul Volcker ended gold’s rally to a then-record $873 by raising borrowing costs to 20 percent in March 1980.

To contact the reporter on this story: Pham-Duy Nguyen in New York at pnguyen@bloomberg.net

To contact the editor responsible for this story: Steve Stroth at sstroth@bloomberg.net. .

Gold-Buying Central Bankers May Extend Record Rally

By Pham-Duy Nguyen - Apr 29, 2011 12:00 PM GMT+0800

Gold prices reached a record 14 times this month on demand from investors seeking an alternative to the dollar after the currency slumped to the lowest since 2009, U.S. debt widened, and the Federal Reserve signaled April 27 that borrowing costs will remain near zero percent for an extended period.

Central banks that were net sellers of gold a decade ago are buying the precious metal to reduce their reliance on the dollar as a reserve currency, signaling demand that may extend a record rally in prices.

As developing countries accelerate purchases, gold may reach $2,000 an ounce this year, compared with a record of $1,538.80 yesterday in New York, said Robert McEwen, the chief executive officer of producer U.S. Gold Corp. Euro Pacific Capital’s Michael Pento, who correctly predicted gold’s highs for the past two years, forecast a 2011 high of $1,600.

Prices reached a record 14 times this month on demand from investors seeking an alternative to the dollar after the currency slumped to the lowest since 2009, U.S. debt widened, and the Federal Reserve signaled April 27 that borrowing costs will remain near zero percent for an extended period. The economy in China, the biggest foreign holder of U.S. Treasuries, grew 9.7 percent in the first quarter.

“China is out to have more gold than America, and Russia is aspiring to the same,” McEwen said yesterday in an interview in New York. “When you have debt, you don’t have a lot of flexibility. China wants to show its currency has more backing than the U.S.”

In 2010, central banks became net buyers for the first time in two decades, adding 87 metric tons in official-sector purchases by countries including Bolivia, Sri Lanka and Mauritius, according to World Gold Council data. China, with more than $3 trillion in foreign-currency reserves, plans to set up new funds to invest in precious metals, Century Weekly reported this week. Russia purchased 8 tons of gold in the first quarter.

China’s Gold Reserves

China, which has just 1.6 percent of its reserves in gold, may invest more than $1 trillion in bullion, Pento said. “China wants to be an international player, and they need to own more gold than they currently have.”

The U.S. Treasury Department projects the government could reach its debt ceiling of $14.3 trillion as soon as mid-May and run out of options for avoiding default by early July. The Fed has kept its benchmark rate between zero percent and 0.25 percent since December 2008 to help stimulate the economy, driving the dollar down 11 percent against a basket of six major currencies during the past year.

“Until monetary policy changes, you’re going to continue to see gold go up,” said Michael Cuggino, who helps manage $12 billion at Permanent Portfolio Funds in San Francisco.

“Ultimately the best thing we can do to create strong fundamentals for the dollar in the medium term is first, keep inflation low, which maintains the buying power of the dollar, and second, create a stronger economy,” Fed Chairman Ben S. Bernanke said on April 27.

U.S. Reserves

As of April, China was the sixth-largest official holder of gold, with 1,054.1 tons, according to World Gold Council estimates. The U.S. has the most, with 8,133.5 tons, or 74.8 percent of the nation’s currency reserves, council data show.

Central-bank buying may have the same impact on gold as the introduction of exchange-traded funds, Cuggino said. Prices have more than tripled since the SPDR Gold Trust, the biggest ETF backed by bullion, was introduced in November 2004.

Central banks in emerging markets may aim to hold 2 percent to 8 percent of their foreign-currency reserves in gold, Francisco Blanch, the head of commodities research at Bank of America Merrill Lynch in New York, said in an interview.

Gold is “close to” its cyclical high, said Blanch, who expects the metal to average $1,500 this year.

Gold’s Enemies

“The enemies of gold are rising interest rates and a balanced budget,” said Pento of Euro Pacific Capital in New York. “I look for a summer swoon once Bernanke exits the bond market. You’re going to have a temporary rise in real interest rates.”

The Fed said it would buy $600 billion in U.S. Treasuries through June.

The Federal Funds rate would have to rise to “Volcker” levels before gold enters a bear market, said Gold Corp.’s McEwen, who expects the metal to rise to $5,000 over three to four years.

Prices have advanced 7.7 percent this year, extending a decade of gains in which gold jumped sixfold from a low in 1999. The all-time inflation adjusted record is $2,338.92, based on the value on Jan. 21, 1980, according to a calculator on the Web site of the Federal Reserve Bank of Minneapolis.

Former Fed Chairman Paul Volcker ended gold’s rally to a then-record $873 by raising borrowing costs to 20 percent in March 1980.

To contact the reporter on this story: Pham-Duy Nguyen in New York at pnguyen@bloomberg.net

To contact the editor responsible for this story: Steve Stroth at sstroth@bloomberg.net. .

People's Bank of China Looking to Diversify into Precious Metals?

People's Bank of China Looking to Diversify Into Precious Metals?

by: Avery Goodman April 28, 2011

Share0 The China Daily, citing another newspaper, the New Century Weekly, says that the Chinese government will diversify its massive $3 trillion dollar foreign reserve stockpiles into investment funds designed to invest in precious metals and oil. New Century says that it got this information from confidential sources inside the Chinese central bank, which is concerned about the continued devaluation of the U.S. dollar and wants to preserve the future buying power of its reserves.

Because a large part of China’s economy is based upon exports, it has been engaged in years of currency debasement of the yuan against the dollar. Successive U.S. administrations, both Democrat and Republican, have uniformly demanded an end to artificial support of the dollar against the yuan and, apparently, the demand has finally been accepted. People really need to be careful what they wish for.

It was, of course, inevitable that the Chinese would wean themselves from over-dependence on exporting to the West. There is no reason to impoverish your own people and restrict their purchasing power for years while using the consequent cheap labor to import technology and know-how, if you never intend to use it.

Ben Bernanke’s bid to out-debase the Chinese has finally borne fruit. China has taken delivery of most of the technology and know-how it is going to get. It is already the factory of the world, producing everything from Barbie dolls to sophisticated automobiles and computers. The remaining technology it would like to import from the West is classified by the military, and America and Europe won’t share it with the Chinese.

China apparently has weighed the alternatives and decided to strike out on its own. It will do everything that it can to become more dependent upon internal, rather than external, demand. It will allow the yuan to rise against the dollar in order to slow down inflation imported from America, and it will make an attempt to salvage whatever value it can from dollar reserves before they become worthless. The plan will come as a surprise for many in the West who assumed that China would not and could not get rid of its dollars, and we do not doubt that many will be in denial until the impact of China’s next move becomes crystal clear.

If China's central bank starts to buy gold, silver, platinum, and palladium on the world market with even a small fraction of its dollar reserves, the impact will be enormous. It means that the demand for U.S. Treasuries as well as European sovereign bonds issuances will fall. That means the U.S. dollar and the euro are going to be deeply declining in their buying power. It also means that the demand for oil and precious metals is going to skyrocket.

Let’s say that China uses 10% of its $3 trillion worth of currency reserves to buy gold. That’s $300 billion. It will buy over 6,000 metric tons of gold at $1540 per ounce. It is interesting to note that, with the gold it already has, plus about 7,000 metric tons more, Chinese gold reserves would equal those of the United States of America.

But the price of gold won’t stay at $1,540 per ounce if the Chinese enter the market in a big way. Nor will the price of silver, platinum and palladium stand still. They will all rise astronomically. Tiny supplies of platinum and palladium, and the fact that both have always been more popular in Far Eastern jewelry than in the West, will conspire to explode those prices if even a small portion of that $300 billion is spent on them.

by: Avery Goodman April 28, 2011

Share0 The China Daily, citing another newspaper, the New Century Weekly, says that the Chinese government will diversify its massive $3 trillion dollar foreign reserve stockpiles into investment funds designed to invest in precious metals and oil. New Century says that it got this information from confidential sources inside the Chinese central bank, which is concerned about the continued devaluation of the U.S. dollar and wants to preserve the future buying power of its reserves.

Because a large part of China’s economy is based upon exports, it has been engaged in years of currency debasement of the yuan against the dollar. Successive U.S. administrations, both Democrat and Republican, have uniformly demanded an end to artificial support of the dollar against the yuan and, apparently, the demand has finally been accepted. People really need to be careful what they wish for.

It was, of course, inevitable that the Chinese would wean themselves from over-dependence on exporting to the West. There is no reason to impoverish your own people and restrict their purchasing power for years while using the consequent cheap labor to import technology and know-how, if you never intend to use it.

Ben Bernanke’s bid to out-debase the Chinese has finally borne fruit. China has taken delivery of most of the technology and know-how it is going to get. It is already the factory of the world, producing everything from Barbie dolls to sophisticated automobiles and computers. The remaining technology it would like to import from the West is classified by the military, and America and Europe won’t share it with the Chinese.

China apparently has weighed the alternatives and decided to strike out on its own. It will do everything that it can to become more dependent upon internal, rather than external, demand. It will allow the yuan to rise against the dollar in order to slow down inflation imported from America, and it will make an attempt to salvage whatever value it can from dollar reserves before they become worthless. The plan will come as a surprise for many in the West who assumed that China would not and could not get rid of its dollars, and we do not doubt that many will be in denial until the impact of China’s next move becomes crystal clear.

If China's central bank starts to buy gold, silver, platinum, and palladium on the world market with even a small fraction of its dollar reserves, the impact will be enormous. It means that the demand for U.S. Treasuries as well as European sovereign bonds issuances will fall. That means the U.S. dollar and the euro are going to be deeply declining in their buying power. It also means that the demand for oil and precious metals is going to skyrocket.

Let’s say that China uses 10% of its $3 trillion worth of currency reserves to buy gold. That’s $300 billion. It will buy over 6,000 metric tons of gold at $1540 per ounce. It is interesting to note that, with the gold it already has, plus about 7,000 metric tons more, Chinese gold reserves would equal those of the United States of America.

But the price of gold won’t stay at $1,540 per ounce if the Chinese enter the market in a big way. Nor will the price of silver, platinum and palladium stand still. They will all rise astronomically. Tiny supplies of platinum and palladium, and the fact that both have always been more popular in Far Eastern jewelry than in the West, will conspire to explode those prices if even a small portion of that $300 billion is spent on them.

Game Plan

Second half of 2011: Overweight commodities, starting energy, base metals, agriculture and precious metals in order of importance.

First half of 2012: Start to diversify into alternatives, commodities and reduce equities. You may wish to buy some investment grade bonds of longer durations.

Second half of 2012: You may need to start shorting equities, go for CTA alternative funds and investment grade bonds of longer duration.

First half of 2013: The blood bath may have started and you may wish to gather ammunition (cash) to buy up residential properties at 30% discount to today's prices.

First half of 2012: Start to diversify into alternatives, commodities and reduce equities. You may wish to buy some investment grade bonds of longer durations.

Second half of 2012: You may need to start shorting equities, go for CTA alternative funds and investment grade bonds of longer duration.

First half of 2013: The blood bath may have started and you may wish to gather ammunition (cash) to buy up residential properties at 30% discount to today's prices.

Friday, 29 April 2011

What to Make of Bernanke's Speech Yesterday

After another long day at work, I was exhausted and was lying on my sofa, half asleep. Bernanke just said that the Fed will keep rates at 0.25% for a few more months. He insisted that inflation is transitory and that the Fed is ready to act when they see signs of peri\sistence in inflation. The fact that the decision to hold rates was unanimous meant that nobody in the FED dared to kill off a nascent economic recovery. After all, unemployment rate was still at 8.8%. The FED won't rest until unemployment falls below 8%.

QE 2 will be allowed to run its course. QE 3 is a possibility if GDP figures turned negative but at the moment unlikely.

I decided that stock markets are likely to be given a lifeline for a few more months. The sectors to target will particularly be precious metals, especially GOLD. So I bought gold call options and bingo, it rose from USD1500/oz to USD1550/oz. Fantastic.

The party may last beyond QE2 because of the low inflation rate in the US and better than expected earnings growth.

QE 2 will be allowed to run its course. QE 3 is a possibility if GDP figures turned negative but at the moment unlikely.

I decided that stock markets are likely to be given a lifeline for a few more months. The sectors to target will particularly be precious metals, especially GOLD. So I bought gold call options and bingo, it rose from USD1500/oz to USD1550/oz. Fantastic.

The party may last beyond QE2 because of the low inflation rate in the US and better than expected earnings growth.

The Results Under Me

So many people got the results that they wanted. If they wanted more, they got it. They never had it so good. Yet they longed for the good old days. I wonder what do they want? Why does the world love the loveable and shallow?? Why can't they scratch beneath the surface and look at substance?

To Climb the Corporate Ladder, You Need More PR Than IQ

I have worked for all kinds of bosses. Some are knowledgeable and have good PR. They are inspirational to work for. Some have no knowledge but can still put up a front. It's all sizzle and no steak. They get threatened easily by subordinates who are more capable than them. They fudge the issue, become biased, put down the more talented and bring up those whom s/he thinks are no threat to them. They often say, "knowledge can be bought". Then there are those who have knowledge but are nasty. They are difficult to work for. But you can learn a lot working for them.

The most important attribute of a boss is one who look at facts and is able to quantify efforts. One who is able to motivate the team. One who will fight for his team when it comes to rewards. One who is not easily threatened by a more talented colleague.

I have been thinking that I need a shift in my value system since I took on a new role. It's more about PR, yet not giving up that good analytical skills that brought me great returns so far in my life. I aim to shift to the first group. The US President Obama is an example of such a leader. God help me become like him.

The most important attribute of a boss is one who look at facts and is able to quantify efforts. One who is able to motivate the team. One who will fight for his team when it comes to rewards. One who is not easily threatened by a more talented colleague.

I have been thinking that I need a shift in my value system since I took on a new role. It's more about PR, yet not giving up that good analytical skills that brought me great returns so far in my life. I aim to shift to the first group. The US President Obama is an example of such a leader. God help me become like him.

Thursday, 28 April 2011

Fed Says Recovery is "Moderate"; Bond Buying to End in June

Fed Says Recovery is ‘Moderate’; Bond Buying to End in June

By Scott Lanman - Apr 28, 2011 1:01 AM GMT+0800

April 26 (Bloomberg) -- Larry Hatheway, chief economist for UBS Investment Bank, talks about the outlook for economic growth in the U.S. and interest rates. He speaks with Maryam Nemazee on Bloomberg Television’s “The Pulse.” (Source: Bloomberg)

Federal Reserve policy makers said the economy is recovering at a “moderate pace” and a pickup in inflation is likely to be temporary, as they agreed to finish $600 billion of bond purchases on schedule in June. (my comments: yes, it's all expected. FED's hands are tied. There won't be a QE3 because inflation expectations are creeping up).

“The economic recovery is proceeding at a moderate pace and overall conditions in the labor market are improving gradually,” the Federal Open Market Committee said today in its statement after a two-day meeting in Washington. “Increases in the prices of energy and other commodities have pushed up inflation in recent months,” and the Fed expects “these effects to be transitory,” the statement said. (my comments: oil price is likely to fall by 10-20% after the middle east crisis).

Chairman Ben S. Bernanke has signaled he’ll maintain record stimulus until job growth accelerates and the recovery is robust enough to withstand tighter credit. The Fed chief has said he expects that a surge this year in fuel and food costs will have only a passing inflationary impact, differing with Fed regional bank presidents who say borrowing costs may need to rise to contain prices.

Stocks rose and the dollar weakened against the euro after the statement. The Dow Jones Industrial Average advanced 0.3 percent to 12,636.51 at 12:53 p.m. in New York. The dollar fell to $1.4696 per euro from $1.4644 late yesterday.

‘Prepared to Adjust’

The Fed, discussing its securities portfolio, said it “is prepared to adjust those holdings as needed to best foster maximum employment and price stability.” Bernanke will discuss the FOMC statement and the panel’s updated economic projections today at his first news conference, scheduled to begin at 2:15 p.m. in Washington.

The FOMC’s characterization of the recovery as “moderate” is similar to the description in the Fed’s Beige Book regional business survey this month and compares with the committee’s March 15 statement saying the economy is on a “firmer footing.”

“The Fed’s view of the world hasn’t changed very much,” Gary Stern, former president of the Minneapolis Fed, said in an interview with Bloomberg Radio. “They continue to emphasize the transitory nature of inflation” and “continue to talk about the economy improving at a moderate pace.”

The Fed left its benchmark interest rate in a range of zero to 0.25 percent, where it’s been since December 2008, and retained a pledge in place since March 2009 to keep it “exceptionally low” for an “extended period.” The central bank will keep reinvesting proceeds of maturing mortgage debt purchased in the first round of large-scale asset purchases that lasted from December 2008 to March 2010. (my comments: FED is likely to keep rates at 0.25% until 2nd half of 2011. Don't count on them to keep it at 0.25% until 2012).

Unemployment ‘Elevated’

“The unemployment rate remains elevated, and measures of underlying inflation continue to be somewhat low, relative to levels that the Committee judges to be consistent, over the longer run, with its dual mandate” for stable prices and maximum employment, the Fed said. The “depressed” housing industry remains a weak spot in the economy, it said.

The Fed repeated that it will “pay close attention to the evolution of inflation and inflation expectations.”

Today’s FOMC decision was unanimous for a third consecutive meeting. Dallas Fed President Richard Fisher and Philadelphia Fed President Charles Plosser, both skeptics of the second round of so-called quantitative easing who voted for the statement today, have suggested they may favor raising interest rates later this year.

Record Stimulus

The Fed’s commitment to record stimulus contrasts with the interest-rate increase this month by the European Central Bank and tightening this year by the biggest emerging-market economies, including China, Brazil and India, which face faster inflation.

Bernanke will become the first Fed chairman to conduct a press briefing following an FOMC decision when he takes the microphone at the Fed’s headquarters. His counterparts in Europe, Japan, the U.K. and Canada already hold regular news conferences.

The press conference, to be broadcast on television and the central bank’s website, marks one of Bernanke’s biggest efforts to improve the Fed’s connections with the public and demystify the institution, which as recently as 1993 didn’t announce its monetary-policy decisions. Bernanke said in February that the central bank was weighing benefits of more transparency against the risk that his remarks would trigger unwanted fluctuations in financial markets.

Projections

The Fed will also release economic projections of governors and regional bank presidents at 2:15 p.m., three weeks sooner than prior practice.

Increases in employment and inflation are helping drive calls to tighten credit. Payrolls have increased by an average 149,000 a month for the past six months, while the unemployment rate has dropped by 1 percentage point since November to 8.8 percent, a two-year low.

Federal Reserve Bank of New York President William C. Dudley, the FOMC’s vice chairman, reiterated in a speech April 1 that a faster pace of job growth is “sorely needed” and that even with 300,000 new jobs per month, the labor market would still have “considerable slack” at the end of 2012. (Don't forget, the FED has a tough task of lowering unemployment).

Janet Yellen, vice chairman of the Fed’s Board of Governors, said April 11 that the increase in food and fuel costs will have only a temporary impact on prices and consumer spending, and warrants no reversal of monetary stimulus.

Food Prices

Food and beverage prices rose in the first quarter by the most since 2008, based on the Labor Department’s Consumer Price Index, while the cost of regular-unleaded gasoline has increased by 26 percent this year to $3.88 a gallon as of yesterday.

The increases helped slow U.S. growth to a 2 percent pace in the first quarter, according to the median estimate of analysts surveyed by Bloomberg News, from 3.1 percent in the prior period. The government releases preliminary figures tomorrow.

The Fed’s preferred price gauge hasn’t flashed a warning. The Commerce Department’s personal consumption expenditures price index, excluding food and energy, rose 0.9 percent in February from a year earlier. Policy makers have a long-run goal for total inflation of about 1.6 percent to 2 percent annually.

Months Away

Economists say the Fed is at least a few months away from starting to reverse the stimulus. Most of the 44 economists surveyed by Bloomberg News from April 20 to April 25 said the central bank this year will probably halt its policy of replacing maturing mortgage debt with Treasuries. The majority of respondents also said the Fed will announce a plan next year of selling mortgage bonds and Treasuries among its assets.

Since the Fed announced the second round of asset purchases on Nov. 3, yields on 10-year Treasuries increased to 3.31 percent as of yesterday from 2.57 percent, while the Standard & Poor’s 500 Index gained 12 percent, yesterday reaching the highest level since June 2008. The dollar weakened by 3.5 percent to the lowest since August 2008 against an index of six currencies.

In a few months, “the data will probably compel them to begin a gradual process of tightening,” Larry Hatheway, chief economist for UBS Investment Bank in London, said in a Bloomberg Television interview before the decision.

“The Fed is still looking essentially at ex-food, ex- energy prices at core, ticking a little higher,” though not enough to raise interest rates now, Hatheway said.

Politicians’ Objections

Bernanke is still seeing objections from politicians within the U.S. and abroad almost six months after the Fed began the unprecedented second round of asset purchases to criticism from Republican politicians and government officials in Germany, China and Brazil.

Senator Mark Kirk, a first-term Republican from Illinois, sent Bernanke a letter on April 25 expressing concern about inflation. He called for an early end to asset purchases should Bernanke “also find the trends that I have now heard widely about.”

Russian Prime Minister Vladimir Putin said last week that compared with the U.S., his country doesn’t have the “same opportunity to make trouble.” The U.S. is “financing the government by using a printing press,” he said.

Some U.S. companies are benefiting from global growth. Atlanta-based United Parcel Service Inc., the world’s largest package-delivery company, yesterday raised its full-year profit forecast after increased international shipping demand pushed first-quarter earnings higher than analysts estimated.

Sporting Goods

Firms are also coping with inflation. Beaverton, Oregon- based Nike Inc., the world’s biggest sporting goods company, said last month it would raise prices. The increases will come on a “wide range of footwear and apparel styles to help mitigate the overall impact of higher input costs,” and the company will carry out “more significant price increases” in 2012, Chief Financial Officer Don Blair said March 17.

Today marked the first time the Fed’s statement was released at about 12:30 p.m. after more than a decade of aiming for 2:15 p.m. The central bank said last month it will provide the statement at 12:30 p.m. during the four two-day meetings when Bernanke has his press conferences and 2:15 p.m. for the other four one-day FOMC meetings.

To contact the reporter on this story: Scott Lanman in Washington at slanman@bloomberg.net.

To contact the editor responsible for this story: Christopher Wellisz at cwellisz@bloomberg.net .

By Scott Lanman - Apr 28, 2011 1:01 AM GMT+0800

April 26 (Bloomberg) -- Larry Hatheway, chief economist for UBS Investment Bank, talks about the outlook for economic growth in the U.S. and interest rates. He speaks with Maryam Nemazee on Bloomberg Television’s “The Pulse.” (Source: Bloomberg)

Federal Reserve policy makers said the economy is recovering at a “moderate pace” and a pickup in inflation is likely to be temporary, as they agreed to finish $600 billion of bond purchases on schedule in June. (my comments: yes, it's all expected. FED's hands are tied. There won't be a QE3 because inflation expectations are creeping up).

“The economic recovery is proceeding at a moderate pace and overall conditions in the labor market are improving gradually,” the Federal Open Market Committee said today in its statement after a two-day meeting in Washington. “Increases in the prices of energy and other commodities have pushed up inflation in recent months,” and the Fed expects “these effects to be transitory,” the statement said. (my comments: oil price is likely to fall by 10-20% after the middle east crisis).

Chairman Ben S. Bernanke has signaled he’ll maintain record stimulus until job growth accelerates and the recovery is robust enough to withstand tighter credit. The Fed chief has said he expects that a surge this year in fuel and food costs will have only a passing inflationary impact, differing with Fed regional bank presidents who say borrowing costs may need to rise to contain prices.

Stocks rose and the dollar weakened against the euro after the statement. The Dow Jones Industrial Average advanced 0.3 percent to 12,636.51 at 12:53 p.m. in New York. The dollar fell to $1.4696 per euro from $1.4644 late yesterday.

‘Prepared to Adjust’

The Fed, discussing its securities portfolio, said it “is prepared to adjust those holdings as needed to best foster maximum employment and price stability.” Bernanke will discuss the FOMC statement and the panel’s updated economic projections today at his first news conference, scheduled to begin at 2:15 p.m. in Washington.

The FOMC’s characterization of the recovery as “moderate” is similar to the description in the Fed’s Beige Book regional business survey this month and compares with the committee’s March 15 statement saying the economy is on a “firmer footing.”

“The Fed’s view of the world hasn’t changed very much,” Gary Stern, former president of the Minneapolis Fed, said in an interview with Bloomberg Radio. “They continue to emphasize the transitory nature of inflation” and “continue to talk about the economy improving at a moderate pace.”

The Fed left its benchmark interest rate in a range of zero to 0.25 percent, where it’s been since December 2008, and retained a pledge in place since March 2009 to keep it “exceptionally low” for an “extended period.” The central bank will keep reinvesting proceeds of maturing mortgage debt purchased in the first round of large-scale asset purchases that lasted from December 2008 to March 2010. (my comments: FED is likely to keep rates at 0.25% until 2nd half of 2011. Don't count on them to keep it at 0.25% until 2012).

Unemployment ‘Elevated’

“The unemployment rate remains elevated, and measures of underlying inflation continue to be somewhat low, relative to levels that the Committee judges to be consistent, over the longer run, with its dual mandate” for stable prices and maximum employment, the Fed said. The “depressed” housing industry remains a weak spot in the economy, it said.

The Fed repeated that it will “pay close attention to the evolution of inflation and inflation expectations.”

Today’s FOMC decision was unanimous for a third consecutive meeting. Dallas Fed President Richard Fisher and Philadelphia Fed President Charles Plosser, both skeptics of the second round of so-called quantitative easing who voted for the statement today, have suggested they may favor raising interest rates later this year.

Record Stimulus

The Fed’s commitment to record stimulus contrasts with the interest-rate increase this month by the European Central Bank and tightening this year by the biggest emerging-market economies, including China, Brazil and India, which face faster inflation.

Bernanke will become the first Fed chairman to conduct a press briefing following an FOMC decision when he takes the microphone at the Fed’s headquarters. His counterparts in Europe, Japan, the U.K. and Canada already hold regular news conferences.

The press conference, to be broadcast on television and the central bank’s website, marks one of Bernanke’s biggest efforts to improve the Fed’s connections with the public and demystify the institution, which as recently as 1993 didn’t announce its monetary-policy decisions. Bernanke said in February that the central bank was weighing benefits of more transparency against the risk that his remarks would trigger unwanted fluctuations in financial markets.

Projections

The Fed will also release economic projections of governors and regional bank presidents at 2:15 p.m., three weeks sooner than prior practice.

Increases in employment and inflation are helping drive calls to tighten credit. Payrolls have increased by an average 149,000 a month for the past six months, while the unemployment rate has dropped by 1 percentage point since November to 8.8 percent, a two-year low.

Federal Reserve Bank of New York President William C. Dudley, the FOMC’s vice chairman, reiterated in a speech April 1 that a faster pace of job growth is “sorely needed” and that even with 300,000 new jobs per month, the labor market would still have “considerable slack” at the end of 2012. (Don't forget, the FED has a tough task of lowering unemployment).

Janet Yellen, vice chairman of the Fed’s Board of Governors, said April 11 that the increase in food and fuel costs will have only a temporary impact on prices and consumer spending, and warrants no reversal of monetary stimulus.

Food Prices

Food and beverage prices rose in the first quarter by the most since 2008, based on the Labor Department’s Consumer Price Index, while the cost of regular-unleaded gasoline has increased by 26 percent this year to $3.88 a gallon as of yesterday.

The increases helped slow U.S. growth to a 2 percent pace in the first quarter, according to the median estimate of analysts surveyed by Bloomberg News, from 3.1 percent in the prior period. The government releases preliminary figures tomorrow.

The Fed’s preferred price gauge hasn’t flashed a warning. The Commerce Department’s personal consumption expenditures price index, excluding food and energy, rose 0.9 percent in February from a year earlier. Policy makers have a long-run goal for total inflation of about 1.6 percent to 2 percent annually.

Months Away

Economists say the Fed is at least a few months away from starting to reverse the stimulus. Most of the 44 economists surveyed by Bloomberg News from April 20 to April 25 said the central bank this year will probably halt its policy of replacing maturing mortgage debt with Treasuries. The majority of respondents also said the Fed will announce a plan next year of selling mortgage bonds and Treasuries among its assets.

Since the Fed announced the second round of asset purchases on Nov. 3, yields on 10-year Treasuries increased to 3.31 percent as of yesterday from 2.57 percent, while the Standard & Poor’s 500 Index gained 12 percent, yesterday reaching the highest level since June 2008. The dollar weakened by 3.5 percent to the lowest since August 2008 against an index of six currencies.

In a few months, “the data will probably compel them to begin a gradual process of tightening,” Larry Hatheway, chief economist for UBS Investment Bank in London, said in a Bloomberg Television interview before the decision.

“The Fed is still looking essentially at ex-food, ex- energy prices at core, ticking a little higher,” though not enough to raise interest rates now, Hatheway said.

Politicians’ Objections

Bernanke is still seeing objections from politicians within the U.S. and abroad almost six months after the Fed began the unprecedented second round of asset purchases to criticism from Republican politicians and government officials in Germany, China and Brazil.

Senator Mark Kirk, a first-term Republican from Illinois, sent Bernanke a letter on April 25 expressing concern about inflation. He called for an early end to asset purchases should Bernanke “also find the trends that I have now heard widely about.”

Russian Prime Minister Vladimir Putin said last week that compared with the U.S., his country doesn’t have the “same opportunity to make trouble.” The U.S. is “financing the government by using a printing press,” he said.

Some U.S. companies are benefiting from global growth. Atlanta-based United Parcel Service Inc., the world’s largest package-delivery company, yesterday raised its full-year profit forecast after increased international shipping demand pushed first-quarter earnings higher than analysts estimated.

Sporting Goods

Firms are also coping with inflation. Beaverton, Oregon- based Nike Inc., the world’s biggest sporting goods company, said last month it would raise prices. The increases will come on a “wide range of footwear and apparel styles to help mitigate the overall impact of higher input costs,” and the company will carry out “more significant price increases” in 2012, Chief Financial Officer Don Blair said March 17.

Today marked the first time the Fed’s statement was released at about 12:30 p.m. after more than a decade of aiming for 2:15 p.m. The central bank said last month it will provide the statement at 12:30 p.m. during the four two-day meetings when Bernanke has his press conferences and 2:15 p.m. for the other four one-day FOMC meetings.

To contact the reporter on this story: Scott Lanman in Washington at slanman@bloomberg.net.

To contact the editor responsible for this story: Christopher Wellisz at cwellisz@bloomberg.net .

Monday, 25 April 2011

Inflation Expectations Continue to Heat Up

by: Calafia Beach Pundit April 08, 2011

As a follow up to a recent post about how the bond market is worrying about inflation, I post these charts. The top chart shows the relationship between 5-yr TIPS and 5-yr Treasuries, with the spread between their real yields (which equates to the market's expectation for the what the CPI will average over the next five years) now within a few bps of an all-time high (2.85%). The second chart does the same for 10-yr maturities, and the spread there has now reached 2.63%, which is also very close to its highest level since 2005.

The message of both charts is the same: Inflation expectations are rising significantly. Fed supporters would be quick to note that this could just be a rational reaction to the recent and continuing rise in oil prices. But Fed critics have more ammunition: The very weak dollar, the broad-based rise in commodity prices, the all-time highs in precious metals, and the substantial rise observed to date in the producer price indices and the ISM prices paid indices.

The message of both charts is the same: Inflation expectations are rising significantly. Fed supporters would be quick to note that this could just be a rational reaction to the recent and continuing rise in oil prices. But Fed critics have more ammunition: The very weak dollar, the broad-based rise in commodity prices, the all-time highs in precious metals, and the substantial rise observed to date in the producer price indices and the ISM prices paid indices.

There is no shortage of evidence that monetary policy is extremely accommodative and inflation pressures are building. The last refuge of the inflation doves (the Phillips Curve theory of inflation) is being dismantled almost daily, as prices all over the world rise even as there remains plenty of slack in the U.S. economy.

To his credit, Dallas Fed President Richard Fisher today sounded a pretty strident inflation alarm: "Inflationary impulses are gaining ground in the rest of the world ... this will result in some unpleasant general price inflation numbers in the next few reporting periods ... there is the risk that we might breach our duty to hold inflation at bay."

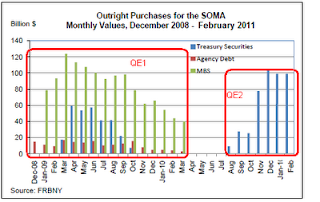

I think it is now clear that the Fed has way overstayed its welcome with QE2, and I find it hard to believe that the rest of the Fed governors will ignore the mounting evidence of such. The ECB has already made the first move to tighten, and meanwhile the figurative rats are abandoning the sinking U.S. dollar (see my prior post on Brazil).

QE2 is scheduled to finish in a few months, but if it is abandoned now it will hardly be cause for concern, since the remaining Treasuries to be bought represent only a very tiny fraction of the total outstanding, and thus are very unlikely to make much of a difference to yields and/or the economy. What will make a difference, of course, is a Fed decision to ignore the evidence of rising inflationary pressures.

My comments:

My comments:

In the last bull cycle, the Fed started hiking rates in June 2004. 5 year inflation expectation was at 2.6%. Now, inflation expectation is at 2.9%. The Fed should have started hiking late 2010. The 10-year UST is around 3.4%. This means that from 0.25% to 3.4%, there are about 13 hikes to go before the yield curve inverts. From Nov 2010 till Dec 2011, that's 13 months of supposed hiking.

The Fed is "way behind the curve". They are 5 months late in their hiking and counting. It will be very difficult for them to control inflation if they hike in 2012. Back in 2004, Alan Greenspan was criticised for acting on inflation too late. This time, Bernanke's far worse.

If the yield curve were to invert in Dec 2011, expect a recession in 2013. The stock market could enter into a bear cycle as late as mid 2012. We have about slightly over a year left in this bull.

by: Calafia Beach Pundit April 08, 2011

As a follow up to a recent post about how the bond market is worrying about inflation, I post these charts. The top chart shows the relationship between 5-yr TIPS and 5-yr Treasuries, with the spread between their real yields (which equates to the market's expectation for the what the CPI will average over the next five years) now within a few bps of an all-time high (2.85%). The second chart does the same for 10-yr maturities, and the spread there has now reached 2.63%, which is also very close to its highest level since 2005.

There is no shortage of evidence that monetary policy is extremely accommodative and inflation pressures are building. The last refuge of the inflation doves (the Phillips Curve theory of inflation) is being dismantled almost daily, as prices all over the world rise even as there remains plenty of slack in the U.S. economy.

To his credit, Dallas Fed President Richard Fisher today sounded a pretty strident inflation alarm: "Inflationary impulses are gaining ground in the rest of the world ... this will result in some unpleasant general price inflation numbers in the next few reporting periods ... there is the risk that we might breach our duty to hold inflation at bay."

I think it is now clear that the Fed has way overstayed its welcome with QE2, and I find it hard to believe that the rest of the Fed governors will ignore the mounting evidence of such. The ECB has already made the first move to tighten, and meanwhile the figurative rats are abandoning the sinking U.S. dollar (see my prior post on Brazil).

QE2 is scheduled to finish in a few months, but if it is abandoned now it will hardly be cause for concern, since the remaining Treasuries to be bought represent only a very tiny fraction of the total outstanding, and thus are very unlikely to make much of a difference to yields and/or the economy. What will make a difference, of course, is a Fed decision to ignore the evidence of rising inflationary pressures.

In the last bull cycle, the Fed started hiking rates in June 2004. 5 year inflation expectation was at 2.6%. Now, inflation expectation is at 2.9%. The Fed should have started hiking late 2010. The 10-year UST is around 3.4%. This means that from 0.25% to 3.4%, there are about 13 hikes to go before the yield curve inverts. From Nov 2010 till Dec 2011, that's 13 months of supposed hiking.

The Fed is "way behind the curve". They are 5 months late in their hiking and counting. It will be very difficult for them to control inflation if they hike in 2012. Back in 2004, Alan Greenspan was criticised for acting on inflation too late. This time, Bernanke's far worse.

If the yield curve were to invert in Dec 2011, expect a recession in 2013. The stock market could enter into a bear cycle as late as mid 2012. We have about slightly over a year left in this bull.

Sunday, 24 April 2011

Good Article About Inflation Expectations

http://seekingalpha.com/article/130417-inflation-expectations-a-primer

Inflation Expectations: A Primer

by: The Baseline Scenario April 09, 2009

By James Kwak

Only a few years ago, the accepted remedy for a recession was for the Federal Reserve to lower interest rates - namely, the Federal funds rate. Now, however, the economy has been stuck in recession for over fifteen months and the Federal funds rate has spent the last several months at zero. (The Fed funds rate cannot ordinarily be negative, because one bank won’t lend $100 to another bank and accept less than $100 in return; it always has the option of just holding onto its $100.) As a result, the Fed has resorted to other policy tools, most notably large-scale purchases of agency and Treasury securities, funded by creating money. (Here’s James Hamilton’s analysis.)

As the Fed’s monetary policy plays a more prominent role in the response to the economic crisis, there will be more talk of inflation or, more accurately, inflation expectations. While inflation is what affects the purchasing power of the money in your wallet, inflation expectations are what affect people’s behavior in ways that have a long-term economic impact. Take the case of wage negotiations, for example: a union that believes inflation will average 5% over the life of a contract will demand higher wage increases than a union that believes inflation will average only 1%. Once those higher wages are built into the contract, the employer is forced to raise prices in order to cover those wage increases, and inflation begins to ripple through the economy.

One of the major objectives of modern monetary policy is to control inflation expectations, because controlling inflation expectations is the first step to controlling inflation. If there is a short-term burst of inflation - as we had a year ago, if you look at headline inflation numbers that include the prices of food and energy - the macroeconomic consequences can be limited if people believe that the Fed can and will bring inflation under control.

Unfortunately, it is impossible to know exactly what people’s inflation expectations are; in fact, it may not even be a sensible question, since different people have different understandings of what inflation is. However, there are three main approaches to estimating inflation expectations.

1. Inflation-indexed government bonds. (If you need a refresher on how a bond works, read the first part of this article.) A traditional bond is a stream of payments that is fixed in nominal terms: for example, $100 in 10 years, and 6% interest, paid semi-annually ($3 every 6 months). Such a bond is not inflation-indexed; if inflation goes up, the purchasing power of that $100 goes down, and it’s too bad for the bondholder.

An inflation-indexed bond, by contrast, pays an amount that is indexed to some measure of inflation. In the U.S., where these bonds are called Treasury Inflation Protected Securities (TIPS), we use the Consumer Price Index. A TIPS bond may have a $100 face value and pay a 2% interest rate. However, every 6 months, that $100 face value is adjusted to reflect the change in the CPI, and the interest payment is calculated as a percentage of the adjusted value of the bond. Then, after 10 years, the bondholder gets back not $100, but $100 times the ratio between the CPI at the end of the period and the CPI at the beginning of the period. This way the bondholder is guaranteed a 2% real return (assuming he paid $100 for the bond), no matter what the rate of inflation is in the interim.

The implied inflation expectation, then, is the difference between the yield on an ordinary bond and the yield on an inflation-indexed bond with the same maturity. If the 5-year Treasury has a yield of 4% and the 5-year TIPS has a yield of 2%, then inflation expectations for the next five years are (about) 2% per year. The reasoning is that in order to buy the regular bond as opposed to the inflation-indexed bond, an investor has to be paid a higher yield to compensate him for the level of inflation that he expects.

Actually, in addition to expected inflation, the Treasury investor also has to be paid an inflation risk premium because, all things being equal, it is better not to have inflation risk than to have it. So the implied inflation expectation is actually slightly less than the spread between the regular and the inflation-indexed bonds. If you didn’t follow that, don’t worry, just remember that, roughly speaking, Treasury yield = TIPS yield + expected inflation.

2. Inflation swaps. These are a type of derivative contract, where the payments under the contract depend on the value of an inflation index, such as the CPI. The swap has a nominal value of, say, $100, but $100 never changes hands. Instead, at the end of some period of time, party A pays party B a fixed rate of interest on $100 - say 2.5% per year. At the end of the period, B pays A the cumulative percentage change in the inflation index over the period. Assuming A has $100 in his pocket, he has now hedged the inflation risk on that $100, because no matter what happens, at the end of the period he will get an amount that compensates him for the impact of inflation on his $100. The price of this hedge is $2.50 per year. (Because these are over-the-counter contracts, there are many variations on this, including swaps with periodic coupon payments.)

For the same reasons described above, the implied inflation expectation is roughly 2.5% per year: party B thinks inflation will be less than 2.5% per year, and therefore is willing to take 2.5% and pay the amount of inflation; party A thinks inflation will be more than 2.5% per year, and therefore is willing to pay 2.5% per year to get the amount of inflation back. So the market clears at 2.5%. (Actually, for the exact same reasons as with bonds - party B has to be paid an inflation risk premium for absorbing the risk in this trade - the inflation expectation is slightly less than 2.5% per year. There are also some complications having to do with the lag in the publication of inflation indices, but let’s ignore that for now.)

One curiosity is that the inflation-indexed bond method and the inflation swap method can produce different estimates. Theoretically this should not happen, because if two products that will have the same price in the long term (since they are based on the same index) have different prices today, there should be an arbitrage opportunity. Why this happens in practice is discussed on pp. 5-6 of this Bank of England paper. (Thanks to Bond Girl for pointing out the paper.)

3. Surveys. You can also just ask people what they think inflation will be. Economists ordinarily prefer markets, under the principle that when people are paying money they are signaling what they really believe. But if you think there are sufficient problems with the markets you may want to go with surveys. Tim Duy has a post with a number of charts, including one of an inflation expectations survey.

So what do things look like today?

This is the historical graph for implied U.S. inflation over the next 5 years, based on TIPS. Remember, you are looking at 5-year inflation expectations as they changed over the last year.

In the dark days of October-December, inflation expectations were clearly negative: that is, the market was expecting deflation over a 5-year period. Things have picked up, but inflation expectations are still around 0.6% - far less than the 1.7-2.0% targeted by the Fed. And that 0.6% is before adjusting for the inflation risk premium, so inflation expectations are actually lower than the chart shows.

And these are current inflation expectations over various time horizons, again derived from inflation-indexed bonds. Note that they are sorted by value, not by time.

TIPS are not very liquid compared to regular Treasury bonds, and the implied inflation expectation numbers are sensitive to aberrations in both the Treasury and the TIPS markets (which have both been pretty aberrant recently). For example, if there is a shortage of TIPS of a given maturity, then the TIPS yields will be artificially low and the implied inflation expectation will be artificially high. Still, it seems like inflation expectations are on the low side, even when it comes to the 10- and 20-year time horizons. (I don’t know what’s going on with the 2-year number: when I look at the underlying bonds, it seems like it should be about -0.1%.)

For more on measuring inflation expectations, there is a short primer from the San Francisco Fed, as well as the Bank of England paper mentioned above.

Inflation Expectations: A Primer

by: The Baseline Scenario April 09, 2009

By James Kwak

Only a few years ago, the accepted remedy for a recession was for the Federal Reserve to lower interest rates - namely, the Federal funds rate. Now, however, the economy has been stuck in recession for over fifteen months and the Federal funds rate has spent the last several months at zero. (The Fed funds rate cannot ordinarily be negative, because one bank won’t lend $100 to another bank and accept less than $100 in return; it always has the option of just holding onto its $100.) As a result, the Fed has resorted to other policy tools, most notably large-scale purchases of agency and Treasury securities, funded by creating money. (Here’s James Hamilton’s analysis.)

As the Fed’s monetary policy plays a more prominent role in the response to the economic crisis, there will be more talk of inflation or, more accurately, inflation expectations. While inflation is what affects the purchasing power of the money in your wallet, inflation expectations are what affect people’s behavior in ways that have a long-term economic impact. Take the case of wage negotiations, for example: a union that believes inflation will average 5% over the life of a contract will demand higher wage increases than a union that believes inflation will average only 1%. Once those higher wages are built into the contract, the employer is forced to raise prices in order to cover those wage increases, and inflation begins to ripple through the economy.

One of the major objectives of modern monetary policy is to control inflation expectations, because controlling inflation expectations is the first step to controlling inflation. If there is a short-term burst of inflation - as we had a year ago, if you look at headline inflation numbers that include the prices of food and energy - the macroeconomic consequences can be limited if people believe that the Fed can and will bring inflation under control.

Unfortunately, it is impossible to know exactly what people’s inflation expectations are; in fact, it may not even be a sensible question, since different people have different understandings of what inflation is. However, there are three main approaches to estimating inflation expectations.

1. Inflation-indexed government bonds. (If you need a refresher on how a bond works, read the first part of this article.) A traditional bond is a stream of payments that is fixed in nominal terms: for example, $100 in 10 years, and 6% interest, paid semi-annually ($3 every 6 months). Such a bond is not inflation-indexed; if inflation goes up, the purchasing power of that $100 goes down, and it’s too bad for the bondholder.

An inflation-indexed bond, by contrast, pays an amount that is indexed to some measure of inflation. In the U.S., where these bonds are called Treasury Inflation Protected Securities (TIPS), we use the Consumer Price Index. A TIPS bond may have a $100 face value and pay a 2% interest rate. However, every 6 months, that $100 face value is adjusted to reflect the change in the CPI, and the interest payment is calculated as a percentage of the adjusted value of the bond. Then, after 10 years, the bondholder gets back not $100, but $100 times the ratio between the CPI at the end of the period and the CPI at the beginning of the period. This way the bondholder is guaranteed a 2% real return (assuming he paid $100 for the bond), no matter what the rate of inflation is in the interim.

The implied inflation expectation, then, is the difference between the yield on an ordinary bond and the yield on an inflation-indexed bond with the same maturity. If the 5-year Treasury has a yield of 4% and the 5-year TIPS has a yield of 2%, then inflation expectations for the next five years are (about) 2% per year. The reasoning is that in order to buy the regular bond as opposed to the inflation-indexed bond, an investor has to be paid a higher yield to compensate him for the level of inflation that he expects.

Actually, in addition to expected inflation, the Treasury investor also has to be paid an inflation risk premium because, all things being equal, it is better not to have inflation risk than to have it. So the implied inflation expectation is actually slightly less than the spread between the regular and the inflation-indexed bonds. If you didn’t follow that, don’t worry, just remember that, roughly speaking, Treasury yield = TIPS yield + expected inflation.

2. Inflation swaps. These are a type of derivative contract, where the payments under the contract depend on the value of an inflation index, such as the CPI. The swap has a nominal value of, say, $100, but $100 never changes hands. Instead, at the end of some period of time, party A pays party B a fixed rate of interest on $100 - say 2.5% per year. At the end of the period, B pays A the cumulative percentage change in the inflation index over the period. Assuming A has $100 in his pocket, he has now hedged the inflation risk on that $100, because no matter what happens, at the end of the period he will get an amount that compensates him for the impact of inflation on his $100. The price of this hedge is $2.50 per year. (Because these are over-the-counter contracts, there are many variations on this, including swaps with periodic coupon payments.)

For the same reasons described above, the implied inflation expectation is roughly 2.5% per year: party B thinks inflation will be less than 2.5% per year, and therefore is willing to take 2.5% and pay the amount of inflation; party A thinks inflation will be more than 2.5% per year, and therefore is willing to pay 2.5% per year to get the amount of inflation back. So the market clears at 2.5%. (Actually, for the exact same reasons as with bonds - party B has to be paid an inflation risk premium for absorbing the risk in this trade - the inflation expectation is slightly less than 2.5% per year. There are also some complications having to do with the lag in the publication of inflation indices, but let’s ignore that for now.)

One curiosity is that the inflation-indexed bond method and the inflation swap method can produce different estimates. Theoretically this should not happen, because if two products that will have the same price in the long term (since they are based on the same index) have different prices today, there should be an arbitrage opportunity. Why this happens in practice is discussed on pp. 5-6 of this Bank of England paper. (Thanks to Bond Girl for pointing out the paper.)

3. Surveys. You can also just ask people what they think inflation will be. Economists ordinarily prefer markets, under the principle that when people are paying money they are signaling what they really believe. But if you think there are sufficient problems with the markets you may want to go with surveys. Tim Duy has a post with a number of charts, including one of an inflation expectations survey.

So what do things look like today?

This is the historical graph for implied U.S. inflation over the next 5 years, based on TIPS. Remember, you are looking at 5-year inflation expectations as they changed over the last year.

In the dark days of October-December, inflation expectations were clearly negative: that is, the market was expecting deflation over a 5-year period. Things have picked up, but inflation expectations are still around 0.6% - far less than the 1.7-2.0% targeted by the Fed. And that 0.6% is before adjusting for the inflation risk premium, so inflation expectations are actually lower than the chart shows.

And these are current inflation expectations over various time horizons, again derived from inflation-indexed bonds. Note that they are sorted by value, not by time.

TIPS are not very liquid compared to regular Treasury bonds, and the implied inflation expectation numbers are sensitive to aberrations in both the Treasury and the TIPS markets (which have both been pretty aberrant recently). For example, if there is a shortage of TIPS of a given maturity, then the TIPS yields will be artificially low and the implied inflation expectation will be artificially high. Still, it seems like inflation expectations are on the low side, even when it comes to the 10- and 20-year time horizons. (I don’t know what’s going on with the 2-year number: when I look at the underlying bonds, it seems like it should be about -0.1%.)

For more on measuring inflation expectations, there is a short primer from the San Francisco Fed, as well as the Bank of England paper mentioned above.

Inflation Expectations Change Stock Market Valuation

My comments: there is a flaw in his valuation. Equity risk premium is the earnings yield in excess of 10-year US Treasury yield, which is around 3.3%. 7.4% - 3.3% is around 4.1%. If you use inflation expectation, fine, it works out to 7.4 - 3.6 = 3.8%. Economic growth should not be included because you're double-counting. Economic growth causes inflation. There is a causal factor which overlaps. You cannot include inflation and then economic growth to calculate ERP.

Today's earnings yield should be 8.4% based on inflation expectation 4.6%. So fair PE should be 11.9x. Hence S&P500 should fall to 1,142. Already, S&P500 is at 1300 plus so you know stocks don't move in lock-step with one single valuation method.

http://seekingalpha.com/article/258261-inflation-expectations-change-stock-market-valuation

Inflation Expectations Change Stock Market Valuation by: Joe Eqcome March 15, 2011

In the past two weeks investors have been rocked by not only political and economic events but also literally by the massive earthquake in Japan sending ripples across the Pacific onto our own shores.

If that weren’t enough to convince you to be careful with regards to equities, you can throw in the coming celestial event of our sun becoming aligned with the center of the Milky Way (a 26,000 year cycle), signaling the end of the Mayan “Long Count” calendar and the end of the world on December 21, 2012 (see movie trailer here). Clearly a “sell” signal.

A More Reasoned Approach: However,for secular investors the current valuation matrix for stocks is more of a concern: the price/earnings ratio (“P/E”). The P/E can alternately be expressed as an earnings’ yield (“E/P”). Let’s for a moment assume a 2011 S&P 500 earnings estimate of $95.98 per share. Based upon the current S&P 500 valuation the earnings yield is 7.4% (13.6 times).

Let’s assume a real US economic growth rate of 2.0% and a consumer inflation expectation of 3.4% which was reported in February by Thomson Reuters/U of Michigan Sentiment Survey. The combination of real growth and inflationary expectation would add up to nominal risk free return of 5.4%. When subtracted from the current implied S&P 500 earnings yield of 7.4% it would imply an equity risk premium of 2.0%.

Getting Ugly? The University of Michigan Survey recently recorded a significant increase in consumer inflation expectation for March. Consumers’ expectation for inflation is now 4.6% up from February’s 3.4%. Now using the same numbers and imputing the new inflation expectation, the S&P 500 earnings yield should now be 8.6% (2.0% + 4.6% + 2.0%) which translates into an 11.6 price/earnings ratio. Based upon the new P/E, the S&P 500 valuation would be 1,113, or off 14.5% from its current valuation.

Take Aways: If QE2 ends when inflation is ramping-up, investment valuations could likely be negatively impacted. Who wins? Equities don’t win; bonds won’t win. If the economy continues to recover with this new inflation expectation, it’s likely that commodities and possibly high quality commercial real estate would be favored under this scenario.

The significantly higher March inflation expectation maybe just an abnormality. Likewise, the equity risk premium may already reflect higher inflation expectations. Either could justify the S&P 500’s current valuations. However, the Fed may just be unrealistic regarding inflation expectations and its ability to respond. As a result it is currently in the process of manufacturing a new bubble to be “pricked”.

Report the Facts: It’s a toss up between inflation and deflation. Inflation is clearly the lesser of two evils--however, nonetheless still evil. To paraphrase Will Rodgers, “I'm not a comedian, I just watch the government and report the facts.” (See the video

Today's earnings yield should be 8.4% based on inflation expectation 4.6%. So fair PE should be 11.9x. Hence S&P500 should fall to 1,142. Already, S&P500 is at 1300 plus so you know stocks don't move in lock-step with one single valuation method.

http://seekingalpha.com/article/258261-inflation-expectations-change-stock-market-valuation

Inflation Expectations Change Stock Market Valuation by: Joe Eqcome March 15, 2011

In the past two weeks investors have been rocked by not only political and economic events but also literally by the massive earthquake in Japan sending ripples across the Pacific onto our own shores.

If that weren’t enough to convince you to be careful with regards to equities, you can throw in the coming celestial event of our sun becoming aligned with the center of the Milky Way (a 26,000 year cycle), signaling the end of the Mayan “Long Count” calendar and the end of the world on December 21, 2012 (see movie trailer here). Clearly a “sell” signal.

A More Reasoned Approach: However,for secular investors the current valuation matrix for stocks is more of a concern: the price/earnings ratio (“P/E”). The P/E can alternately be expressed as an earnings’ yield (“E/P”). Let’s for a moment assume a 2011 S&P 500 earnings estimate of $95.98 per share. Based upon the current S&P 500 valuation the earnings yield is 7.4% (13.6 times).

Let’s assume a real US economic growth rate of 2.0% and a consumer inflation expectation of 3.4% which was reported in February by Thomson Reuters/U of Michigan Sentiment Survey. The combination of real growth and inflationary expectation would add up to nominal risk free return of 5.4%. When subtracted from the current implied S&P 500 earnings yield of 7.4% it would imply an equity risk premium of 2.0%.

Getting Ugly? The University of Michigan Survey recently recorded a significant increase in consumer inflation expectation for March. Consumers’ expectation for inflation is now 4.6% up from February’s 3.4%. Now using the same numbers and imputing the new inflation expectation, the S&P 500 earnings yield should now be 8.6% (2.0% + 4.6% + 2.0%) which translates into an 11.6 price/earnings ratio. Based upon the new P/E, the S&P 500 valuation would be 1,113, or off 14.5% from its current valuation.

Take Aways: If QE2 ends when inflation is ramping-up, investment valuations could likely be negatively impacted. Who wins? Equities don’t win; bonds won’t win. If the economy continues to recover with this new inflation expectation, it’s likely that commodities and possibly high quality commercial real estate would be favored under this scenario.

The significantly higher March inflation expectation maybe just an abnormality. Likewise, the equity risk premium may already reflect higher inflation expectations. Either could justify the S&P 500’s current valuations. However, the Fed may just be unrealistic regarding inflation expectations and its ability to respond. As a result it is currently in the process of manufacturing a new bubble to be “pricked”.

Report the Facts: It’s a toss up between inflation and deflation. Inflation is clearly the lesser of two evils--however, nonetheless still evil. To paraphrase Will Rodgers, “I'm not a comedian, I just watch the government and report the facts.” (See the video

The Big Challenges of the Future

Sometimes, I lay awake at night thinking of what the future holds. We have the following challenges: exploding population, escalating food prices, global warming, escalating oil prices, rising sea levels, lack of clean drinking water.

Perhaps one factor that has been ignored is the future of labour markets. Robotics are getting more advanced. In future, all repetitive jobs will be done by robots. In 10 - 20 years, more complex tasks can be done by robots too. When we order food from McDonalds in 10 years' time, a robotic kiosk could be serving us. The staff cooking our burgers could be robots. The ones clearing our tables could be roving robots. THe only humans who are working will probably be programmers, mechanical engineers and a manager just to make sure things are ok.

What will happen to us humans? Surgeries will be conducted by robots. Human doctors merely steer mechanical hands. Unemployment will sky rocket. Company profits will sky rocket. But who will have a salary to buy those goods? In 10 years time, the divide between the highly skilled and the redundant will be very wide. Perhaps through taxes, the government will have to give handouts to its citizens, who in turn become customers. It is a very fuzzy future.

Perhaps one factor that has been ignored is the future of labour markets. Robotics are getting more advanced. In future, all repetitive jobs will be done by robots. In 10 - 20 years, more complex tasks can be done by robots too. When we order food from McDonalds in 10 years' time, a robotic kiosk could be serving us. The staff cooking our burgers could be robots. The ones clearing our tables could be roving robots. THe only humans who are working will probably be programmers, mechanical engineers and a manager just to make sure things are ok.

What will happen to us humans? Surgeries will be conducted by robots. Human doctors merely steer mechanical hands. Unemployment will sky rocket. Company profits will sky rocket. But who will have a salary to buy those goods? In 10 years time, the divide between the highly skilled and the redundant will be very wide. Perhaps through taxes, the government will have to give handouts to its citizens, who in turn become customers. It is a very fuzzy future.

US' 10 yr Inflation Expectations at 1.94%, Unbelievable

According to Cleveland Fed, inflation is expected to be around 1.94% in 10 years' time. It's incredible and unbelievable. This is one of the data that the US Fed Reserve watch closely. With such low expectations, it is unlikely that the Fed will hike rates soon. The Producer Price Index is around 1.7%, and CPI at 1.1% last month. How could crude oil price at USD127/bbl not trigger inflation is quite staggering.

When US stocks peaked in Nov 2007, oil price was at SGD140/bbl. Using SGD as a common denominator and calibrated by around 3% of inflation per annum, today's oil price is around SGD124/bbl. We are a whisker away from tragedy.