As we outlined in detail on October 5, a quick fix to satisfy the markets is unlikely to materialize in Europe. According to the Wall Street Journal:

“The news stories about a big-bang recapitalization of EU banks are overdone,” says Sony Kapoor of Re-Define, a financial think tank he has set up. “The EU has neither the money, nor the political will for action on such a scale.” Indeed, German Chancellor Angela Merkel implicitly recognized in Brussels on Wednesday that there is no consensus that a European-wide recapitalization is necessary, points out Stephen Lewis of Monument Securities in London. The German government was ready to recapitalize German banks, she said, “if there is a general view that the banks are not sufficiently capitalized.”

Bloomberg notes bank recapitalization does not address the root of the problems in Europe:

Even a recapitalization of European banks may fail to reassure investors because they will still question the ability of governments to meet their borrowing costs. Injecting capital into Europe’s banks won’t provide the “silver bullet” that is needed to solve the crisis, said Huw van Steenis, a banking analyst at Morgan Stanley in London. It needs to be done in conjunction with measures to shore up sovereign debt, he said. “The banking crisis isn’t going to be resolved until the sovereign crisis is resolved,” said David Watts, a strategist at CreditSights Inc. in London. “Capital isn’t the way to go because the needs are too big and will weaken the sovereign.” Banks would need to raise about 148 billion euros in the event of a 60 percent writedown on their holdings of Greek debt, 40 percent for Portugal and Ireland and 20 percent for Italy and Spain, Kian Abouhossein a JPMorgan Chase & Co. analyst, wrote in a note to clients Sept. 26.

The bears have control of both the short and long-term trends. The chart below is as of Thursday’s close. There is nothing particularly bullish about it. Price is below the 50-day (red); it closed below the 20-day (blue) on Friday. Both the 50-day and 20-day have negative slopes, which is bearish. The green parallel trendlines have impacted price since early April - they all have bearish slopes. The pink parallel trendlines have impacted price since the August 8 low - they, too, have bearish slopes. Price faces possible resistance from the 50-day and the twin trendlines near 1,181.

Commodities and precious metals have been flashing deflationary and bearish signals in recent months. Stocks and commodities did not perform well in the period August-November 2008. Using this link, compare the chart of the silver ETF SLV in 2008 to the present day. The charts give specific bull/bear levels to monitor in SLV.

{kind=link}

The Dexia Bank bailout highlights the scope of the problems with bad debt. Dexia ironically passed the recent stress tests with flying colors; according to the Financial Times “it not only passed the exercise, it emerged as one of the safest banks in Europe”. Bloomberg reported on October 8:

While France and Belgium have rushed to protect their local units, hurdles to an agreement remain as they wrestle over responsibility for assets hit by the crisis that has caused the bank’s short-term funding to evaporate. Dexia’s troubled assets are being folded into a “bad bank” and could amount to as much as 190 billion euros ($256 billion).

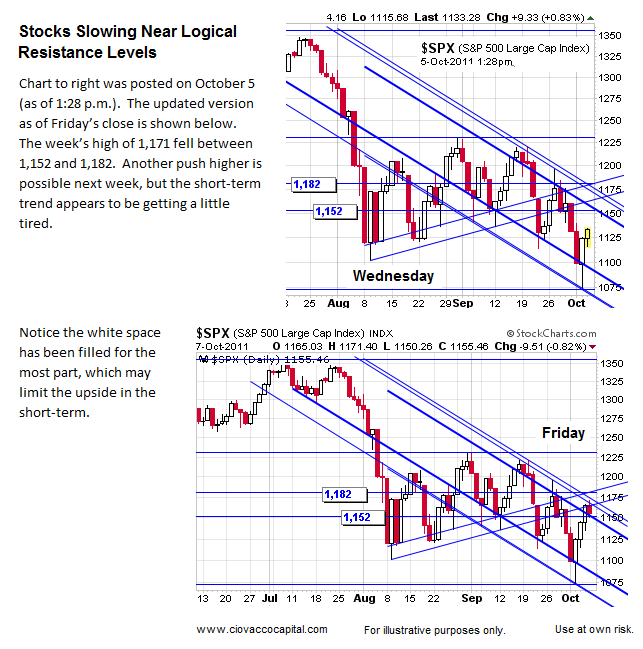

The S&P 500 stalled on Friday at logical resistance levels after Italy’s and Spain’s debt ratings were cut. The ratings changes brought the problems in Europe back to the forefront of investors’ minds. If the bears maintain control of the market, we will continue to favor a menu of deflation-friendly assets as outlined on October 4, including bonds (TLT), the dollar (UUP), and shorts (SH).

{kind=link}