The most important story as we head into the new week - from Bloomberg:

Germany said European Union leaders won’t provide the complete fix to the euro-area debt crisis that global policy makers are pushing for at an Oct. 23 summit. German Chancellor Angela Merkel has made it clear that “dreams that are taking hold again now that with this package everything will be solved and everything will be over on Monday won’t be able to be fulfilled,” Steffen Seibert, Merkel’s chief spokesman, said at a briefing in Berlin today. The search for an end to the crisis “surely extends well into next year.”

Equity And Credit Markets Telling Two Different Stories

October 16,

2011 |

Since the stock markets bottomed on October 4th, the S&P 500 has rallied

nearly 14% in less than two weeks. Given the strength of the rally one would

expect to see other markets confirm such a dramatic move. However, this is not

the case as the credit markets do not show the same enthusiasm with credit

spreads still elevated in the face of economic and financial risk. One of these

markets is wrong and one is right, with a resolution ahead.

Mixed Messages

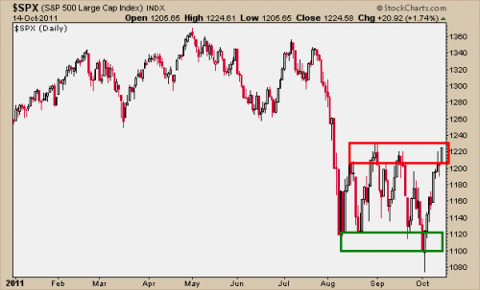

After Friday ’s close the S&P 500 has retraced a fair amount of its prior decline and is now back up to the top of its trading range since August, and is down 2.63% year-to-date. It seems hope springs eternal as rumors of Europe taking swifter action ahead of their banking and sovereign debt crises gives the global equity markets a bid. It will be interesting to see what the S&P 500 does from here as it is bottom-up against resistance and some kind of pullback should be expected.

Source: StockCharts.com

Mixed Messages

After Friday ’s close the S&P 500 has retraced a fair amount of its prior decline and is now back up to the top of its trading range since August, and is down 2.63% year-to-date. It seems hope springs eternal as rumors of Europe taking swifter action ahead of their banking and sovereign debt crises gives the global equity markets a bid. It will be interesting to see what the S&P 500 does from here as it is bottom-up against resistance and some kind of pullback should be expected.

[click to enlarge]

Source: StockCharts.com

While the market's advance over the last two weeks

has been perceived by many to give the all-clear in terms of European financial

risk or a US recession ahead, I wouldn’t be so sure. What should give investors

pause is that leading economic indicators often act coincidentally with the

stock market, meaning they tend to move in concert as both discount future

economic trends. Thus, when they do not move in harmony it typically means one

of the two is about to play catch up with the other.

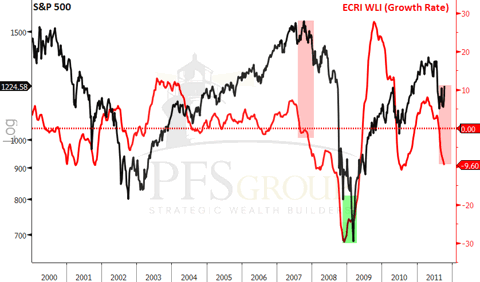

Shown below is the Economic Cycle Research

Institute’s (ECRI) Weekly Leading Index (WLI) which shows a negative 9.6%

smoothed growth rate, a level last seen in the mild 2001 recession as well as in

early 2008 and the middle of 2010. With readings this negative it isn’t

surprising the ECRI is calling for another recession (“U.S. Economy Tipping into Recession”), their first recession

call since 2008. While many were calling for another recession last year given

the weak WLI, ECRI actually stated we would skirt a recession as their

longer-leading indicators were still heading up. Now their WLI, which is more of

an intermediate indicator, is moving in the same direction as their long-leading

indicators with both heading south, which is why they are making a

high-conviction recession call this time around.

[click to enlarge]

Source: Bloomberg

As seen above, the two prior periods of divergence

proved to be key turning points in the market. In 2007 the WLI continued to head

south while the S&P 500 rallied into October. Closing out the year the

S&P 500 caught up with the WLI as it was correctly forecasting a major turn

in the economy ahead of what the S&P 500 was discounting. Likewise, at the

end of the last bear market and

recession the WLI bottomed in 2008 ahead of the March 2009 bottom in the S&P

500 and was forecasting future improvement in the economy. Last year when the

S&P 500 rallied after its summer correction, so too did the WLI fail to

confirm the market’s move. So, the fact that the S&P 500 has rallied

nearly 14% since its low earlier in the month and yet the WLI has continued to

decline should give equity investors pause as the two have, once again,

diverged.

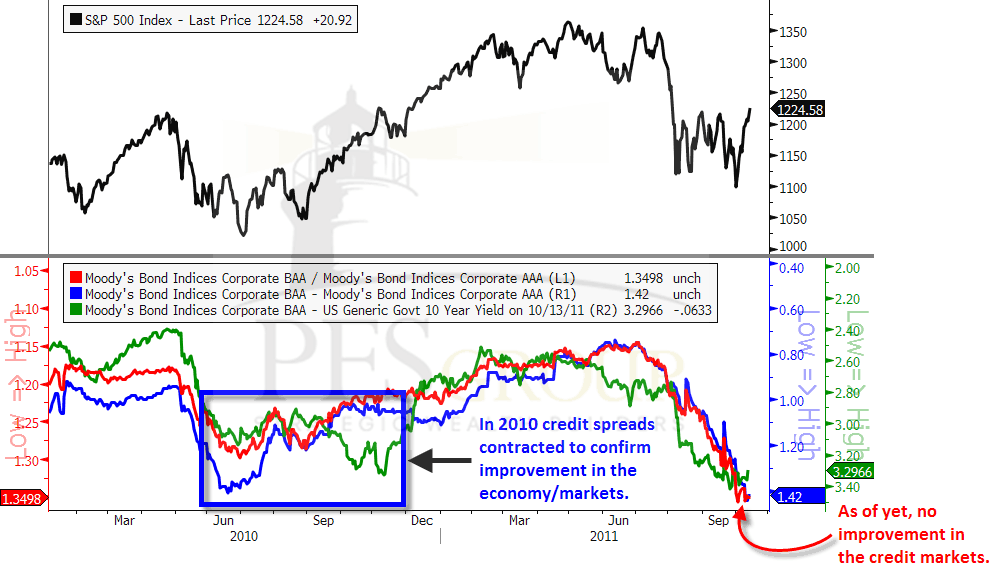

Not only are leading economic indicators not

confirming the stock market’s move, neither are the credit markets. Shown below

is the S&P 500 on the top panel and below are several bond market credit

spreads, inverted for directional similarity. As you can see, last year when the

stock market advanced after its summer correction various bond spreads began to

contract to signal credit risk was easing. Credit risk began to pick up again in

the middle of this year just as the stock market was peaking. Please note,

however, that while the S&P 500 has been in a trading range since August,

each rally we've experienced has not been confirmed by easing credit spreads,

leading to a subsequent failure to breakout of the trading range in each case.

Since the S&P 500 peak this summer, we have just witnessed one of the

largest uninterrupted rallies, and since we have seen virtually no improvement

in credit spreads, I think this rally is highly suspect and investors should

remain cautious.

[click to enlarge]

Source: Bloomberg

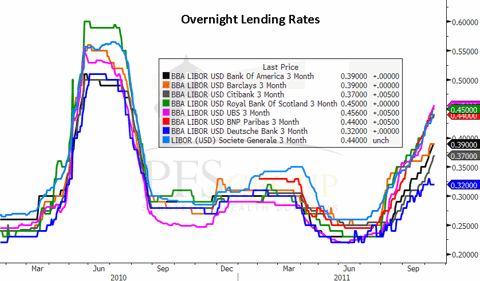

In addition to bond market credit spreads not

confirming the stock market, neither are bank overnight lending rates which

continue to rise even in the face of a sharply rising stock market. Back in June

2010 overnight lending rates peaked as credit risk began to stabilize and then

in July and August overnight lending rates plummeted and global financial risks

began to subside. This time around overnight lending rates for European and U.S.

banks continue to climb and show no sign of stabilization.

[click to enlarge]

Source: Bloomberg

Until we see the leading economic indicators and the

credit markets singing the same tune as the stock market, the recent stock

market rally should be viewed with a great deal of skepticism.

Disclosure: I have no positions in

any stocks mentioned, and no plans to initiate any positions within the next 72

hours.