Top 5 Graphs of the Week: Japan, U.S., Monetary Policy in EM

This week we look at some of the latest economic data coming out of Japan; noting a rare occurrence of positive inflation, and observing a further trade deficit in April. Then we look at some U.S. data, first checking in on the U.S. consumer sentiment index, and then a proxy for investor sentiment - long term mutual fund flows. Finally, the latest monetary policy interest rate decisions are covered-off.

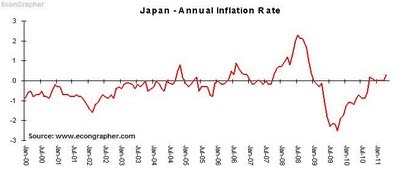

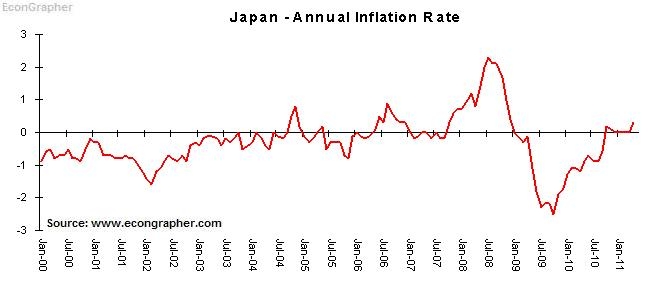

1. Japan Inflation

As noted Japan recorded a rare positive inflation figure in April as consumer prices rose 0.3% on an annual basis, having sat at 0% for most of this year, while April 2010 saw deflation of -1.2%. A certain degree of the positive inflation figure can be attributed to temporary shortages brought about by the earthquake, but inflation had been in a mild upward trajectory anyway. Like the rest of the world, Japan had seen some impact from rising commodity prices (as can be seen in the upward trend in imports on the next chart). Meanwhile, aggregate demand has probably only had a marginal impact on inflation as the Japanese economy has been in its second recession after a brief period of growth.

Click to enlarge

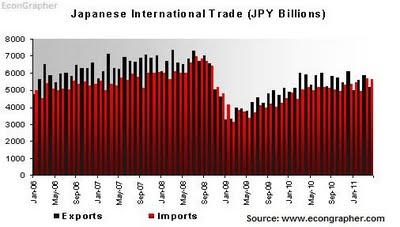

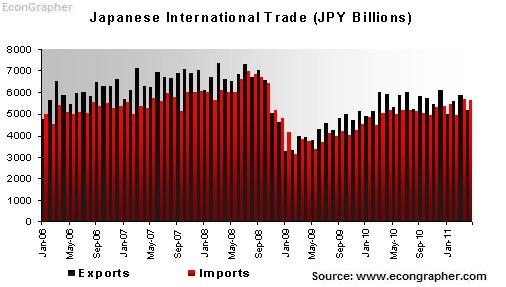

2. Japan International Trade

Japan reported exports of JPY 5.2 trillion in the month of April, down -13% year on year and -12% month on month. Imports were JPY 5.6 trillion, up 9% from April last year and down -1% compared to March. The April figures add another month of trade deficit as rising import costs meet relatively stable exports. The April figures did see some impact from the earthquake, as supply chain disruptions weighed on exports. Overall, Japan is yet to see either its exports or imports reach pre-crisis levels, which shows the weakness of the Japanese economy, but also the slow rate of growth and economic recovery in its trading partners (not to mention a rising share of global exports for China and other emerging markets).

Click to enlarge

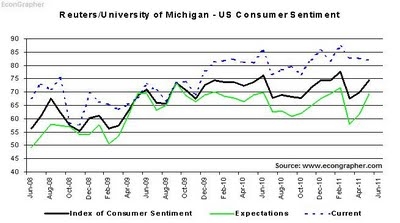

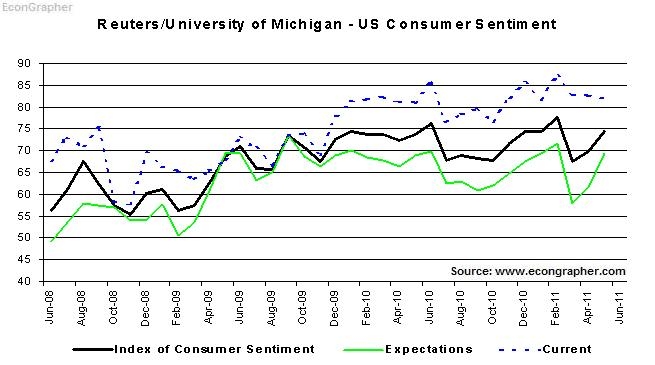

3. U.S. Consumer Sentiment

The Reuters/University of Michigan U.S. consumer sentiment survey showed some improvement in the final reading for May, with the index at 74.3 vs consensus 72.4, and the April reading of 69.8. Future expectations performed well, at 69.5 vs 61.6 in April, meanwhile current conditions was basically flat at 81.9 vs 82.5 in the previous month. So while the current conditions result was not inspiring, the trajectory of the future expectations part was promising, indeed if the trajectory continues it will be positive for the medium term outlook, which is consistent with other indicators and conditions.

Click to enlarge

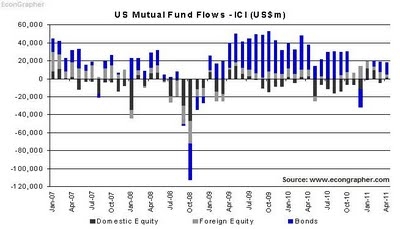

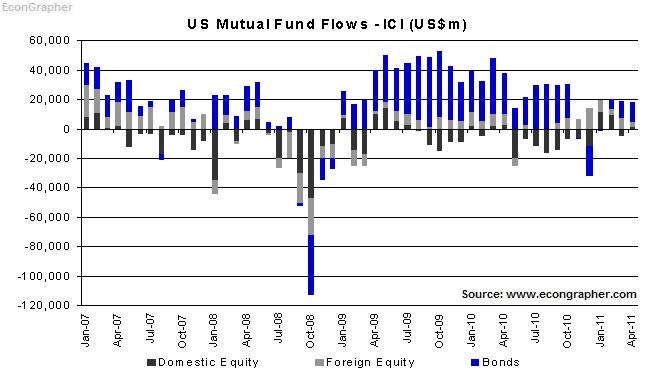

4. U.S. Mutual Fund Flows

U.S. mutual fund flows remained in positive territory in total during April, with the majority of net inflows going to bond mutual funds, showing a possible pick up in momentum after flows into bond funds dried up at the start of the year. Domestic equity flows continued to languish, while foreign equity fund flows remained positive as investors looked elsewhere for better macro-economic fundamentals. It will pay to watch this chart through the year, especially as key events unfold such as the ending of quantitative easing, and a potential short-term correction in U.S. equities. A final thought on the chart below is the large amount of funds that have flown into bond mutual funds, this aspect will be interesting for equities when / if bond returns begin to suffer as the monetary policy stance turns later this year.

Click to enlarge

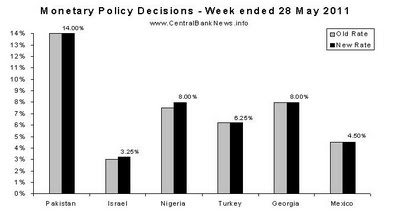

5. Monetary Policy Review

The past week in monetary policy saw six emerging market central banks announce interest rate decisions. Those that altered interest rate levels included: Israel +25bps to 3.25%, and Nigeria +50bps to 8.00%, while those that held interest rates unchanged were: Pakistan 14.00%, Turkey 6.25%, Georgia 8.00%, and Mexico 4.50%. So it was very much a continuation of the theme where emerging markets begin to take more caution in balancing the growth vs inflation risks, but also as the inflation impulse begins to taper off as policy measures and stable commodity prices begin to take effect. But the rate hikes in Israel and Nigeria show that inflation pressures are not completely gone in emerging markets, indeed Vietnam is still a hotspot of inflation.

Click to enlarge

Summary

So we saw the emergence of inflation in Japan, after a long period of deflation, however short term factors were likely the main cause of this. Meanwhile, Japan's international trade results showed stagnant growth and short term impact from the earthquake. In the U.S., consumer sentiment improved again heading in a promising trajectory. Also in the U.S., long term mutual fund flows pointed to some interesting trends, and some key areas to watch in the stock and bond markets through the rest of the year. Finally, the week in monetary policy saw two emerging market economies tighten, while other emerging markets opted for caution in the growth risk vs inflation risk balancing act.

1. Japan Inflation

As noted Japan recorded a rare positive inflation figure in April as consumer prices rose 0.3% on an annual basis, having sat at 0% for most of this year, while April 2010 saw deflation of -1.2%. A certain degree of the positive inflation figure can be attributed to temporary shortages brought about by the earthquake, but inflation had been in a mild upward trajectory anyway. Like the rest of the world, Japan had seen some impact from rising commodity prices (as can be seen in the upward trend in imports on the next chart). Meanwhile, aggregate demand has probably only had a marginal impact on inflation as the Japanese economy has been in its second recession after a brief period of growth.

Click to enlarge

2. Japan International Trade

Japan reported exports of JPY 5.2 trillion in the month of April, down -13% year on year and -12% month on month. Imports were JPY 5.6 trillion, up 9% from April last year and down -1% compared to March. The April figures add another month of trade deficit as rising import costs meet relatively stable exports. The April figures did see some impact from the earthquake, as supply chain disruptions weighed on exports. Overall, Japan is yet to see either its exports or imports reach pre-crisis levels, which shows the weakness of the Japanese economy, but also the slow rate of growth and economic recovery in its trading partners (not to mention a rising share of global exports for China and other emerging markets).

Click to enlarge

3. U.S. Consumer Sentiment

The Reuters/University of Michigan U.S. consumer sentiment survey showed some improvement in the final reading for May, with the index at 74.3 vs consensus 72.4, and the April reading of 69.8. Future expectations performed well, at 69.5 vs 61.6 in April, meanwhile current conditions was basically flat at 81.9 vs 82.5 in the previous month. So while the current conditions result was not inspiring, the trajectory of the future expectations part was promising, indeed if the trajectory continues it will be positive for the medium term outlook, which is consistent with other indicators and conditions.

Click to enlarge

4. U.S. Mutual Fund Flows

U.S. mutual fund flows remained in positive territory in total during April, with the majority of net inflows going to bond mutual funds, showing a possible pick up in momentum after flows into bond funds dried up at the start of the year. Domestic equity flows continued to languish, while foreign equity fund flows remained positive as investors looked elsewhere for better macro-economic fundamentals. It will pay to watch this chart through the year, especially as key events unfold such as the ending of quantitative easing, and a potential short-term correction in U.S. equities. A final thought on the chart below is the large amount of funds that have flown into bond mutual funds, this aspect will be interesting for equities when / if bond returns begin to suffer as the monetary policy stance turns later this year.

Click to enlarge

5. Monetary Policy Review

The past week in monetary policy saw six emerging market central banks announce interest rate decisions. Those that altered interest rate levels included: Israel +25bps to 3.25%, and Nigeria +50bps to 8.00%, while those that held interest rates unchanged were: Pakistan 14.00%, Turkey 6.25%, Georgia 8.00%, and Mexico 4.50%. So it was very much a continuation of the theme where emerging markets begin to take more caution in balancing the growth vs inflation risks, but also as the inflation impulse begins to taper off as policy measures and stable commodity prices begin to take effect. But the rate hikes in Israel and Nigeria show that inflation pressures are not completely gone in emerging markets, indeed Vietnam is still a hotspot of inflation.

Click to enlarge

Summary

So we saw the emergence of inflation in Japan, after a long period of deflation, however short term factors were likely the main cause of this. Meanwhile, Japan's international trade results showed stagnant growth and short term impact from the earthquake. In the U.S., consumer sentiment improved again heading in a promising trajectory. Also in the U.S., long term mutual fund flows pointed to some interesting trends, and some key areas to watch in the stock and bond markets through the rest of the year. Finally, the week in monetary policy saw two emerging market economies tighten, while other emerging markets opted for caution in the growth risk vs inflation risk balancing act.

No comments:

Post a Comment