In Equity Markets - 'It's the Earnings, Stupid'

Political strategist James Carville famously stated, “It’s the economy stupid,” during the 1992 presidential campaign. Despite a historic record approval rating of 90 by President George H.W. Bush after the 1991 Gulf War victory, Bush Sr. still managed to lose the election to President Bill Clinton because of a weak economy. President Barack Obama would serve himself well to pay attention to history if he wants to enter the “two-termer” club. Pundits are placing their bets on Obama due to his large campaign war chest, a post-Osama bin Laden extinguishment approval bump, and a cloudy Republican candidate weather forecast. If however, the unemployment rate remains elevated and the current administration ignores the spending/debt crisis, then the President’s re-election hopes may just come crashing down.

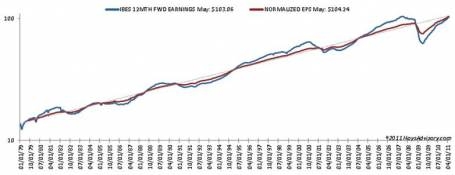

Price Follows Earnings

The similarly vital relationship between the economy and politics applies to the relationship of earnings and the equity markets too. Instead of the key phrase, “It’s the economy stupid,” in the stock market, “It’s all about the earnings stupid” is the crucial guideline. The balance sheet may play a role as well, but at the end of the day, the longer-term trend in stock prices eventually follows earnings and cash flows (i.e., investors will pay a higher price for a growing stream of earnings and a lower price for a declining or stagnant stream of earnings). Ultimately, even value investors pay more attention to earnings in the cases where losses are deteriorating or hemorrhaging (e.g. a Blockbuster or Enron). Another main factor in stock price valuations is interest rates. Investors will pay more for a given stream of earnings in a low interest rate environment relative to a high interest rate environment. Investors lived through this in the early 1980s when stocks traded at puny 7-8x P/E ratios due to double-digit inflation and a Federal Funds rate that peaked near 20%.

(Click chart to expand)

Source: HaysAdvisory.com – S&P 500 earnings growth keeps chugging along despite worries.Bears Come Out of Hibernation

Source: HaysAdvisory.com – S&P 500 earnings growth keeps chugging along despite worries.Bears Come Out of Hibernation

Today, earnings portray a different picture relative to the early eighties. Not only are S&P 500 (SPY) operating earnings growing at a healthy estimated rate of +17% in 2011, but the 10-year Treasury note is also trading at a near-record low yield of 3.06%. In spite of these massively positive earnings and cash flow dynamics occurring over the last few years, the recent -3% pullback in the S&P 500 index from a month ago has awoken some hibernating bears from their caves. Certainly a slowing or pause in the overall economic indicators has something to do with the newfound somber mood (i.e., meager Q1 real GDP growth of +1.8% and rising unemployment claims). Contributing to the bears’ grumpy moods is the economic debt hangover we are recovering from. However, a large portion of the fundamental economic expansion experienced by corporate America has not been fueled by the overwhelming debt still being burned off throughout the financial sector and eventually our federal and state governments. Companies have become leaner and meaner – not only paying down debt, but also increasing dividends, buying back stock, and doing more acquisitions. The corporate debt-free muscle is further evidenced by the $100 billion in cash held by the likes of IBM, Microsoft Corp. (MSFT), and Google Inc. (GOOG) – and still growing.

At a 13.5x P/E multiple of 2011 earnings, perhaps the stock market is pricing in an earnings slowdown? But as of last week, about 70% of the S&P 500 companies reporting Q1 earnings have exceeded expectations. If this trend continues, perhaps we will see James Carville on CNBC rightfully shouting the maxim, “It’s the earnings, stupid!”

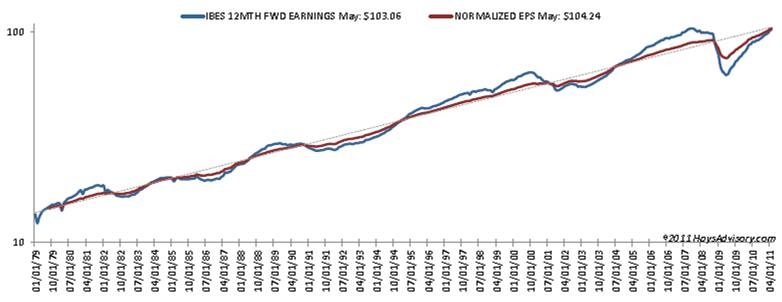

Price Follows Earnings

The similarly vital relationship between the economy and politics applies to the relationship of earnings and the equity markets too. Instead of the key phrase, “It’s the economy stupid,” in the stock market, “It’s all about the earnings stupid” is the crucial guideline. The balance sheet may play a role as well, but at the end of the day, the longer-term trend in stock prices eventually follows earnings and cash flows (i.e., investors will pay a higher price for a growing stream of earnings and a lower price for a declining or stagnant stream of earnings). Ultimately, even value investors pay more attention to earnings in the cases where losses are deteriorating or hemorrhaging (e.g. a Blockbuster or Enron). Another main factor in stock price valuations is interest rates. Investors will pay more for a given stream of earnings in a low interest rate environment relative to a high interest rate environment. Investors lived through this in the early 1980s when stocks traded at puny 7-8x P/E ratios due to double-digit inflation and a Federal Funds rate that peaked near 20%.

(Click chart to expand)

Source: HaysAdvisory.com – S&P 500 earnings growth keeps chugging along despite worries.

Source: HaysAdvisory.com – S&P 500 earnings growth keeps chugging along despite worries.Today, earnings portray a different picture relative to the early eighties. Not only are S&P 500 (SPY) operating earnings growing at a healthy estimated rate of +17% in 2011, but the 10-year Treasury note is also trading at a near-record low yield of 3.06%. In spite of these massively positive earnings and cash flow dynamics occurring over the last few years, the recent -3% pullback in the S&P 500 index from a month ago has awoken some hibernating bears from their caves. Certainly a slowing or pause in the overall economic indicators has something to do with the newfound somber mood (i.e., meager Q1 real GDP growth of +1.8% and rising unemployment claims). Contributing to the bears’ grumpy moods is the economic debt hangover we are recovering from. However, a large portion of the fundamental economic expansion experienced by corporate America has not been fueled by the overwhelming debt still being burned off throughout the financial sector and eventually our federal and state governments. Companies have become leaner and meaner – not only paying down debt, but also increasing dividends, buying back stock, and doing more acquisitions. The corporate debt-free muscle is further evidenced by the $100 billion in cash held by the likes of IBM, Microsoft Corp. (MSFT), and Google Inc. (GOOG) – and still growing.

At a 13.5x P/E multiple of 2011 earnings, perhaps the stock market is pricing in an earnings slowdown? But as of last week, about 70% of the S&P 500 companies reporting Q1 earnings have exceeded expectations. If this trend continues, perhaps we will see James Carville on CNBC rightfully shouting the maxim, “It’s the earnings, stupid!”

No comments:

Post a Comment